A Guide on VA Loan Debt-to-Income (DTI) Ratio

Your debt-to-income ratio, or DTI, is an important factor lenders consider when you apply for a VA mortgage loan. Learn more in this extensive guide.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

As a veteran or military member, you have access to one of the best home loan programs around: the VA loan.

Meeting the VA’s service requirements is a significant step, but lenders also assess factors like your debt-to-income ratio (DTI) to ensure you can comfortably manage your monthly mortgage payments. If your DTI is higher, it may mean you’ll qualify for a smaller loan amount, potentially requiring you to consider a less expensive home.

Key Takeaways

- Your DTI ratio shows lenders what portion of your income goes toward debt.

- Two DTI types exist: front-end (mortgage payment) and back-end (all debts).

- VA guidelines suggest a maximum DTI, but exceeding it doesn’t automatically disqualify you.

- Lowering your DTI can improve loan approval chances.

What Is Debt-To-Income (DTI) Ratio?

Your debt-to-income ratio, or DTI, is an important factor lenders consider when you apply for a mortgage loan. This number reflects how much of your monthly income your debts take up (specifically, the minimum payment on those debts).

Most loan programs have a maximum DTI to stay at or under to qualify, and lenders can even use DTI to set your interest rate. VA loans don’t have a specific DTI maximum, but it does encourage lenders to look more carefully at borrowers with DTIs over a certain threshold.

Front-End DTI Vs. Back-End DTI

There are two types of DTI lenders look at: front-end and back-end. Your front-end DTI is how much of your income would go to your monthly mortgage payment. So, for instance, if you have a mortgage of $2,000 and a monthly income of $4,000, you’d have a front-end DTI of 50%.

The back-end DTI is a more comprehensive number that shows how much of your income all your debts account for. Using the above example, if you had a mortgage of $2,000, a minimum credit card payment of $250, and a student loan payment of $750, you’d have a DTI of 75% ($3,000 / $4,000).

| Front-end DTI | Back-end DTI |

| Includes only your housing payment Helps lenders assess whether you have enough income to cover your new mortgage | Includes your housing payment and all other monthly debts Gives lenders a more comprehensive overview of your finances |

Debt-to-Income Ratio for VA Home Loan

The Department of Veterans Affairs recommends that borrowers have a DTI of 41% or less to qualify for a VA loan, but it doesn’t outright say that borrowers with DTIs higher than this will be denied.

Qualifying for a VA loan is still possible if you have a DTI over 41%. The underwriter just needs to look more carefully at your application to justify approving your loan.

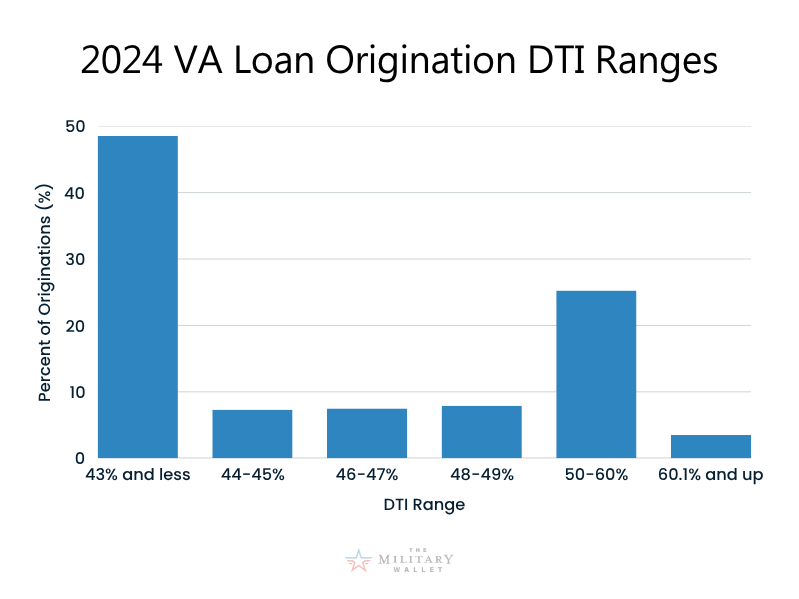

According to HMDA data, 49% of VA home loan originations in 2024 were for borrowers with a DTI ratio of 43% or less:

How Other Finances Can Impact Loan Approvals

Lenders use more than just DTI to assess your financial capabilities. Your credit score and history with managing debt play a big role too, so if you have a high DTI, a high credit score and spotless credit report can help sway things in your direction.

DTI Ratio and Residual Income

Having more residual income can also help your case. Residual income is money left over after paying your debts each month. Your lender will require a certain amount of it to qualify for a loan.

If you have 20% more than that limit, it could offset your high DTI. For example, if the lender normally requires at least $1,000 in residual income, you can make up for your high DTI by having $1,250 instead.

How Do You Calculate Debt-to-Income Ratio for VA Loan?

To calculate your DTI, you need a list of your debts and all the minimum payments they come with. You also need to know how much gross income you bring in each month.

Note: Gross income is the total amount of money you earn each month before any deductions, like taxes, health insurance premiums, or retirement contributions. It’s essentially your income on paper before any expenses are accounted for.

See below for an example of how to calculate DTI:

| Debt | Cost |

| Student loan payment | $300 |

| Car payment | $500 |

| Credit card payment | $150 |

| Estimated new mortgage payment | $2,000 |

| Total monthly debts | $2,950 |

| Monthly income | $8,000 |

| Front-end DTI (Estimated new mortgage payment / Monthly income) | 25% |

| Back-end DTI (Total monthly debts / Monthly income) | 37% |

How do I lower DTI for my VA Home Loan?

To lower your DTI, pay down your debts more aggressively — particularly on revolving debt, like credit cards. This will lower your monthly payment, reducing your DTI. If you can pay off a debt entirely (say, your car loan), that could be even more effective.

You can also work to increase your income. This might mean taking on some freelance work or a side gig or asking for more hours or a raise at work.

Finally, you could also restructure your debt. Sometimes, consolidating all your debts to a single loan can help reduce your interest rate and your total monthly payments which would also reduce your DTI.

Related Posts

- VA Loan Rates: Compare Today’s VA Home Loan Rates

- VA Loan Spouse Requirements

- VA Loan Eligibility Requirements

- VA Loan Inspection Requirements & Appraisal Checklist

- Guide to VA Appraisal Fees and Process