5 Reasons to Choose a Roth IRA over a Traditional IRA

If you're in the military, you're used to TSP. As you transition, you might consider a Roth IRA. Learn why to choose Roth IRA over a Traditional IRA.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

Reason #1: You Don’t Need a Deduction Now.

You may choose to invest in a Roth IRA if you don’t need the tax savings right now, and plan to be in a higher tax bracket when you start withdrawing from your IRA. When you compare a traditional and a Roth IRA, the biggest difference is when you realize tax savings. Since a traditional IRA allows you to take an immediate tax break on your contribution, it makes sense for people who are in high income brackets (over 25%).Reason #2: You Plan to be in a Similar or Lower Tax Bracket

Most servicemembers and families are in lower tax brackets, especially those with members who routinely deploy to combat zones. When these members retire, they might realize a slight increase in their tax liability due to the loss of their allowances. However, that increase usually will keep them in the same tax bracket. If you expect to use your post-military career ramp up your net worth, you should pay the taxes now. That way, you can enjoy tax-free growth in your retirement years. This decision requires a lot of thought about how you envision the rest of your life.Reason #3: You plan to have more assets than you can use in your lifetime.

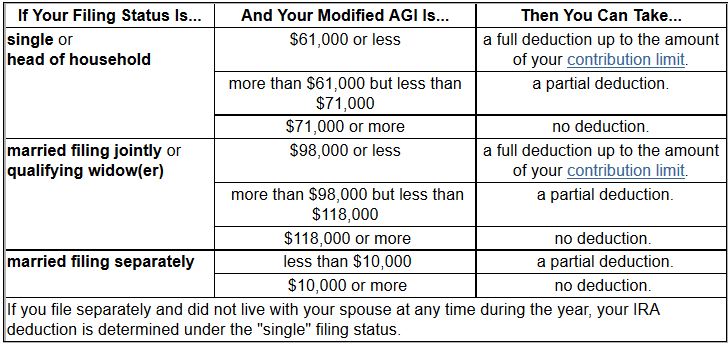

If you’re tracking with reasons #1 & #2, then you might end up in a position where you achieve financial independence fairly early. In that case, it’s worth considering what you’ll do with the money you’ve accumulated. Here’s another key difference between traditional & Roth IRAs. With a traditional IRA, you’ll have to start taking required minimum distributions (RMDs) after you’ve reached 73. If you already have enough income to support your lifestyle, then your worry becomes more about how to minimize your tax liability. While there are several things you can do to minimize your tax liability with RMDs, it’s much easier to avoid them. When you choose a Roth IRA, you don’t have to take RMDs. Ever. The money is there when you need it. However, you can let it grow tax free for the rest of your life without being forced to withdraw it.Reason #4: You’re covered by a workplace retirement plan, and your income is above the deduction limit for a traditional IRA.

This probably will not happen while you’re on active duty, but it could happen during your post-military career. There are no income limits for traditional IRA contributions. However, the IRS limits the deductibility of those contributions if either you or your spouse is covered by a workplace retirement plan. The impact is that if you are covered by a workplace retirement plan, and your income is above a certain threshold, your deduction might only be partially deductible or not deductible at all.

If you leave the military, you should be aware of:

The impact is that if you are covered by a workplace retirement plan, and your income is above a certain threshold, your deduction might only be partially deductible or not deductible at all.

If you leave the military, you should be aware of:

- The availability of a qualified workplace retirement plan

- Your expected adjusted gross income (AGI)

Reason #5: You plan to generate cash flow from your IRA to support your living expenses

A lot of people use the following savings plan:- Save as much money as possible during working years

- Figure out what to do with that money after retirement