Roth Conversions: Why Timing Matters for Military Members

The tax-equivalency principle shows that when you pay taxes on retirement savings matters just as much as how you save, and military members have a unique advantage when it comes to timing Roth conversions.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

Editor’s Note: The tax bracket figures used in this article reflect pre-2018 tax law. The Tax Cuts and Jobs Act of 2017 replaced these brackets with a new structure (10%, 12%, 22%, 24%, 32%, 35%, 37%) that has since been made permanent. The tax-equivalency principles and concepts discussed here remain accurate regardless of which specific brackets apply to your situation.

- The tax-equivalency principle states that as long as tax rates remain the same, a traditional IRA and a Roth IRA will yield identical after-tax values. The timing of when taxes are paid does not matter if the rate stays constant.

- Roth conversions are most valuable when done at lower tax rates, if your tax rate rises in retirement, converting to a Roth earlier at a lower rate results in more after-tax wealth.

- Military members are uniquely positioned to benefit from Roth conversions early in their careers, when non-taxable allowances like BAH and BAS keep their effective tax bracket lower than their total compensation would suggest.

There is an ever-old discussion on the importance of saving for retirement. And ever since the Roth IRA was created by the Taxpayer Relief Act of 1997, there’s been a similar discussion on whether you should contribute to a traditional IRA or a Roth IRA. Finally, there has been just as much discussion on whether you should convert current traditional accounts to Roth accounts.

Since most people are eligible to take a tax deduction on their IRA contribution, this involves paying taxes on the conversion amount, then transferring the remainder to their Roth account. However, many factors can determine how beneficial Roth conversions can be.

This article aims to discuss:

- Tax-equivalency principle

- The impact of tax rate changes on account values

- Why tax rates might change over time

- When you might take advantage of changing tax brackets to maximize account value

- When you might not want to make Roth conversions to preserve value

What Is the Tax-Equivalency Principle?

What’s the tax-equivalency principle? Simply put, it states that as long as tax rates remain the same, two tax-advantaged accounts will yield the same after-tax amount, regardless of whether the contribution was taxed upon contribution or withdrawal.

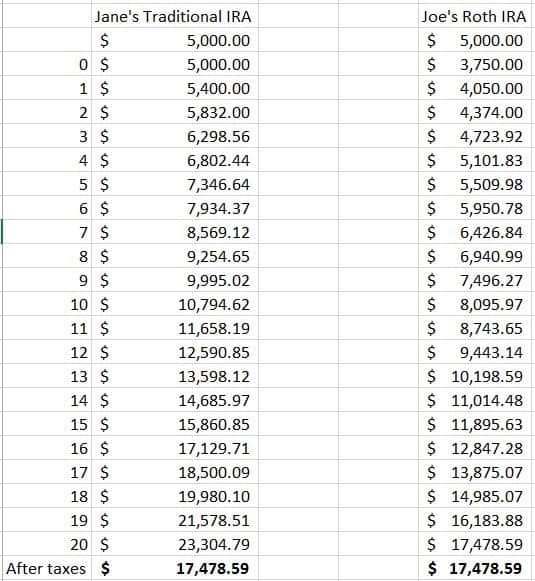

For example, Jane and Joe each have $5,000 in traditional IRAs. Jane decides to keep her traditional, and Joe into a Roth. Both are in the 25% tax bracket and remain so over time. They also make identical investments. Since Jane made her contribution on a pre-tax basis, she starts off with $5,000. Joe has to pay taxes on his contribution, so he only starts with $3,750 ($5,000 minus 25%).

Let’s fast forward 20 years when they plan to withdraw from their accounts. Their identical investments have achieved an average annual return of 8%. Jane would have $23,304.79, while Joe would only have $17,478.59. However, when you tax Jane’s pre-tax IRA at 25%, her account ends up at $17,478.59, the same as Joe’s. That’s the tax-equivalency principle: Assuming identical investments remain at the same tax rate over time, it doesn’t matter whether the contribution is taxed or the withdrawal is taxed.

For military members, this principle takes on added significance. Non-taxable allowances like BAH and BAS effectively lower your taxable income, often placing you in a lower tax bracket than your total compensation would suggest. This makes the early years of a military career, when taxable income is relatively low, an especially valuable window for Roth conversions or Roth IRA contributions. Paying taxes at a lower rate now, rather than a potentially higher rate in retirement, is the core advantage the tax-equivalency principle illustrates.

Of course, most people do not stay in the same tax bracket forever, so let’s look at what happens when tax rates change over time.

How Rising Tax Rates Impact Roth Conversions

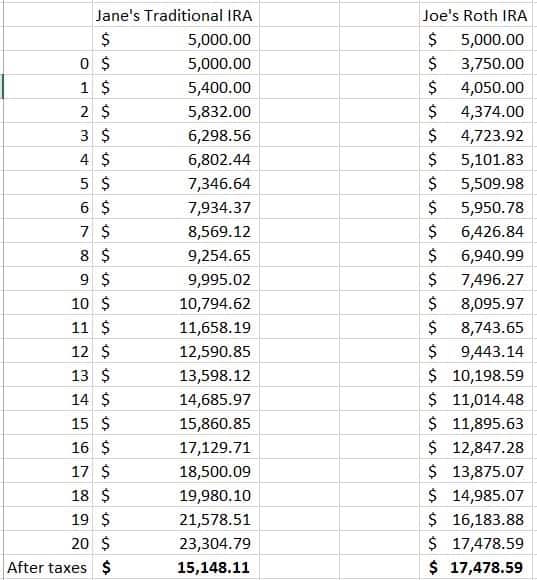

Using the previous example, let’s say Joe and Jane are wildly successful over the course of their careers. Instead of staying in the 25% tax bracket, they eventually move up to the 35% bracket. How would this change their after-tax values?

Joe’s account value would stay the same-$17,478.59 since the change in tax bracket has no impact on his Roth account. However, Jane’s account would only be worth $15,148.11 after taxes. In this case, Joe paid taxes on his account at 25%, which allowed him to avoid paying taxes at 35% later on.

How Falling Tax Rates Impact Roth Conversions

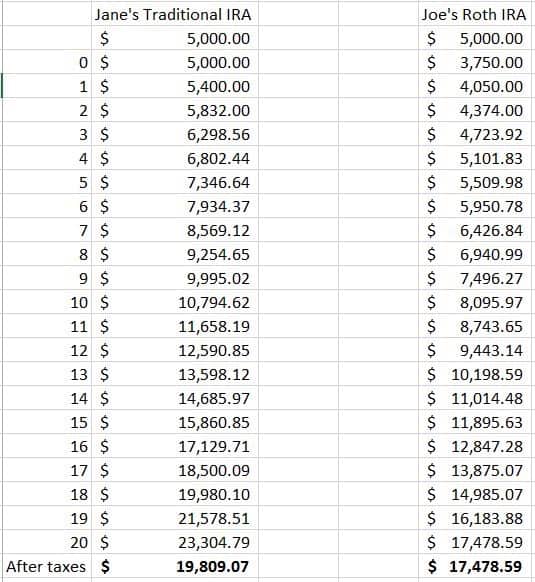

Instead of moving into the 35% tax bracket, let’s assume Joe and Jane retire and move into the 15% tax bracket. How does their after-tax value change?

Joe’s account would still stay the same at $17,478.59. However, Jane’s after-tax account value is now $19,809.07. This makes sense because Jane only had to pay 15% on her account, whereas Joe paid 25% up front.

Key Takeaways: When to Make Roth Conversions

In both cases, the difference in account values reflects the impact of the change in the marginal tax rate on investment returns. The key point is that maximizing account values depends on making conversions at low tax rates and avoiding conversions at high tax rates.

Understanding when tax rates are likely to change over the course of your career is the key to maximizing the value of Roth conversions. For military members, this planning is especially important given the unique tax advantages of military service, including the impact of non-taxable allowances on your effective tax bracket.