How to Convert a Roth IRA at Vanguard – An Illustrated Tutorial

This tutorial shows you how to convert a Traditional IRA to a Roth IRA at Vanguard. The screenshots make it easy to convert your Roth IRA in about 5 minutes.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

You have a lot of choices when it comes to retirement planning. From employer-sponsored accounts, such as a 401k or 403b, to the Individual Retirement Account, or IRA. These accounts come in different flavors too. You can decide when you want to pay your taxes – either now (Traditional 401k or IRA) or in the future (Roth 401k or IRA). These decisions can have a profound impact on your overall retirement planning.

Of course, these accounts come with certain conditions, such as income eligibility, annual contribution limits, and other conditions. So you need to do your research to optimize your retirement accounts and minimize your taxes, either today or in the future.

And that is exactly what we will look at today: how to convert a Traditional IRA to a Roth IRA at Vanguard.

What is a Roth IRA Conversion?

A Quick primer:

Simply put, a Roth IRA conversion is when you convert, or transfer, your investments from a Traditional IRA to a Roth IRA. This changes how your retirement account will be taxed when you make withdrawals. Contributions to Traditional IRAs are made pre-tax, and withdrawals are taxed when made in retirement. Contributions to a Roth IRA are made after taxes have been withheld, and withdrawals are tax-free in retirement. Learn more about the differences between Roth and Traditional IRAs.

Why convert? Taxes, taxes, taxes. And flexibility.

Converting a Traditional IRA to a Roth IRA – Assumptions in this Guide

This website isn’t about tax planning, so you must research before proceeding with this tutorial. We will assume that you know the tax implications of converting to a Roth IRA and that you have already decided this is the course of action you wish to take.

If you are still deciding, I recommend reading this primer on Roth IRA conversions so you can understand what they are, how they work, and the impact they may have on your taxes. Of course, consulting with a financial planner or tax professional is never a bad idea for further guidance.

This guide is also specific to Vanguard, though the process may be similar at other financial institutions. I simply chose to cover Vanguard because I already have an IRA there. I recommend looking into some of our recommended options for opening a Roth IRA if you don’t already have a Roth IRA (Vanguard is listed, as are several other major mutual fund firms and discount brokerages).

How to Convert a Traditional IRA to a Roth IRA at Vanguard

Here is how to do it at Vanguard:

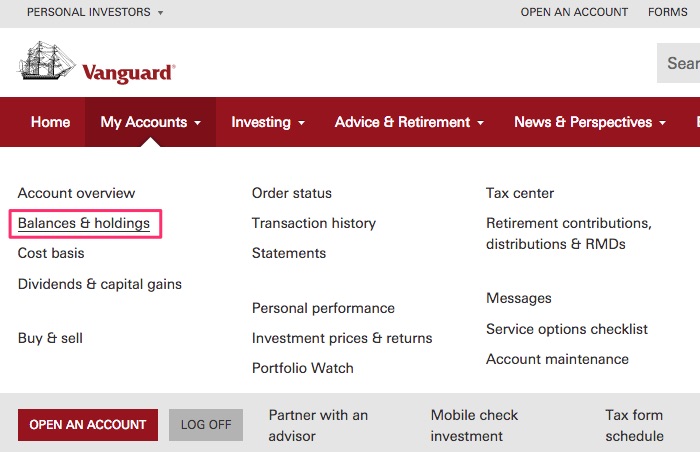

Step 1. Visit the Balances and Holdings Page in Your Vanguard Account

You can navigate to your Balances &Holdings page by clicking the link at the top of your navigation bar. See the screenshot for an image of the drop-down. Click the link, and you will see a list of all your accounts, including each account’s balance and its holdings.

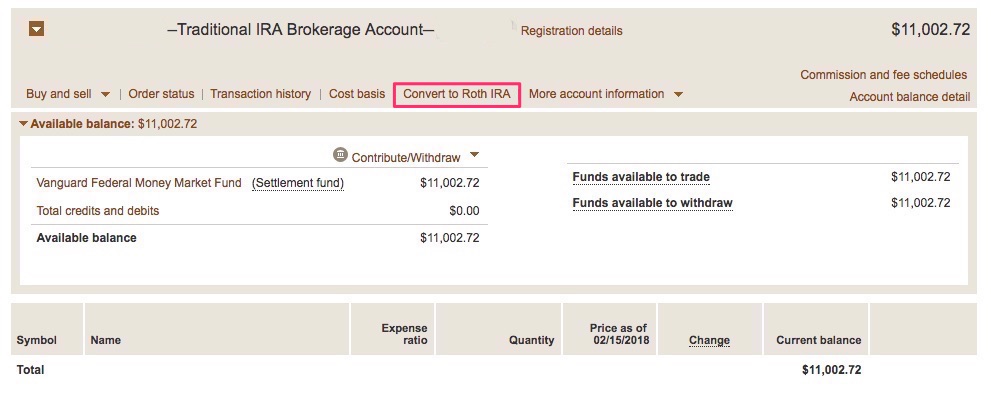

Step 2. Find your Traditional IRA Account and Click the Covert to IRA Link

You should see the account name and description and several links for actions you can take, such as Buy and Sell, Order Status, Transaction History, etc. Click the link, Convert to Roth IRA.

This will take you to the Roth IRA Conversion page.

Here is the screenshot of the link to click:

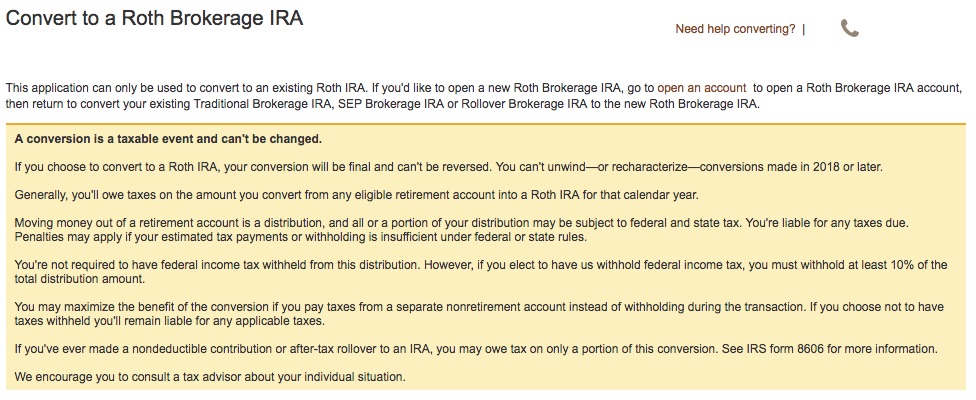

Step 3. Visit the Roth IRA Conversion Page

You need to confirm you want to convert your Traditional IRA to a Roth IRA, and you are aware of the potential tax consequences. The latter is a huge factor, and you don’t want to wait until the last minute to decide if a Roth IRA conversion is right for you.

The Roth IRA Conversion Page will have a large notice at the top informing you that a Roth IRA conversion is a taxable event and cannot be changed. Before 2018, it was possible to recharacterize or unwind a Roth IRA conversion. This could be used to strategically unwind the Roth IRA and recharacterize it as a Traditional IRA if it lost value. The taxpayer could later convert it back to a Roth IRA if they wanted to, but at a lower tax basis. As you can imagine, the paperwork trail could be onerous!

However, recharacterizing the conversion is no longer allowed. In other words, this is a final decision with no take-backs!

Text:

A conversion is a taxable event and can’t be changed.

If you choose to convert to a Roth IRA, your conversion will be final and can’t be reversed. You can’t unwind—or recharacterize—conversions made in 2018 or later.

Generally, you’ll owe taxes on the amount you convert from any eligible retirement account into a Roth IRA for that calendar year.

Moving money out of a retirement account is a distribution, and all or a portion of your distribution may be subject to federal and state tax. You’re liable for any taxes due. Penalties may apply if your estimated tax payments or withholding is insufficient under federal or state rules.

You’re not required to have federal income tax withheld from this distribution. However, if you elect to have us withhold federal income tax, you must withhold at least 10% of the total distribution amount.

You may maximize the benefit of the conversion if you pay taxes from a separate nonretirement account instead of withholding during the transaction. If you choose not to have taxes withheld, you’ll remain liable for any applicable taxes.

If you’ve ever made a nondeductible contribution or after-tax rollover to an IRA, you may owe tax on only a portion of this conversion. See IRS form 8606 for more information.

We encourage you to consult a tax advisor about your individual situation.

Step 4. Choose Which Account to Convert

This decision is made for you if you only have one Traditional IRA. But many Vanguard customers have an IRA in a Vanguard Mutual Fund account, and some have them in a Vanguard Brokerage account. The difference? You can trade any security inside the Brokerage account. You can only trade Vanguard securities inside the mutual fund account. It’s also possible to have multiple IRAs with Vanguard if you did an IRA rollover from a 401k or another retirement account, or if you inherited an IRA.

You may have to make more than one conversion if you have more than one Traditional IRA with Vanguard. The process is the same. You would simply repeat the steps for the other account(s).

Remember that you will receive a Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., from Vanguard for each account you convert to a Roth IRA. These forms will be sent out at the beginning of the following calendar year and will also be sent to the IRS.

So you will need to take the appropriate action when you file your taxes the following year. If your Traditional IRA was a tax-deductible IRA, you would have to pay taxes on the amount you convert. If your Traditional IRA was of the non-deductible variety, you would only pay taxes on the gains, not the contributions.

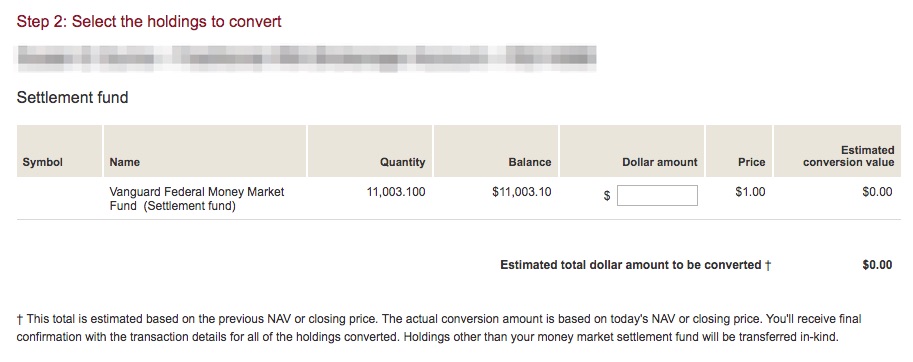

Choose Which Shares to Convert: After selecting which account to convert, you must also decide which shares to convert. In the above screenshot, I chose to “Convert all of the account.” However, you can elect to choose some, or all, of the account. If you choose to do a partial conversion, you will see something like this:

As you can see from the screenshots above, the balance from this conversion was $11,003.10, which represents a non-deductible Traditional IRA contribution for two tax years, plus a partial month’s interest. The $11,000.00 will not be taxed on the conversion, but the $3.10 will be considered a taxable distribution. So I will need to pay taxes on the $3.10.

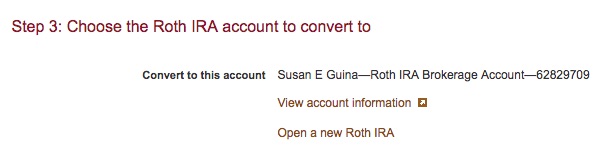

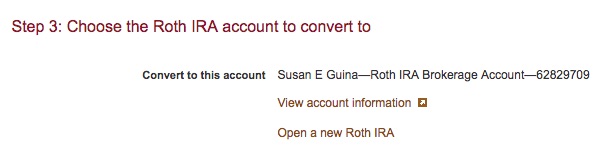

Step 5. Choose Which Account to Convert to

This is very similar to the step above. You may only have one Roth IRA with Vanguard. If so, it will already be selected as the default account when you convert to a Roth IRA. However, you will have to choose which Roth IRA to convert your Traditional to if you have more than one account.

Vanguard will also not allow you to access this page without having a Roth IRA. You will be prompted to create a Roth IRA account if you don’t already have one when you click the “Convert to Roth IRA” link from Step 2.

Choose your destination Roth IRA, then move to the next step.

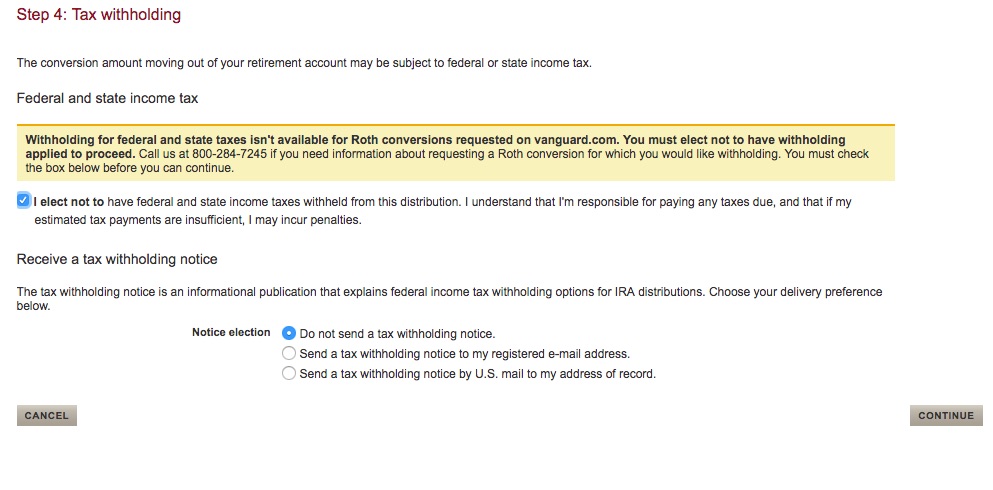

Step 6. Choose Your Tax Withholding

Converting a Roth IRA is considered a distribution of your Traditional IRA. The good news is you’re not required to have state or federal income tax withheld from your distribution (Roth IRA conversion). However, if you elect to have us withhold federal income tax, you must withhold at least 10% of the total distribution amount.

Let that last bit sink in. If you choose to have your taxes withheld, Vanguard will withhold at least 10% of your distribution.

The better way to maximize your Roth IRA conversion is to pay any taxes from a non-retirement account. This keeps more of your money in your Roth IRA where it can compound over time and will grow tax-free. Of course, it will also give you more tax-free retirement withdrawals.

You will still owe taxes on the distribution, but you can decide how you want to pay them. That is a very powerful tool.

A Note About Back Door Roth IRA Conversions: As noted above, this particular Roth IRA conversion was from a non-deductible Traditional IRA. It’s important to file IRS Form 8606 with your taxes each year you make any non-deductible contributions, so there is no confusion on the cost-basis of your distribution. In my case, I had two years’ worth of Traditional IRA contributions plus a small amount of interest. In my case, only the gains will be considered a taxable distribution.

How should you handle the tax withholding section?

The Vanguard representative suggested clicking the radio button for electing not to have federal and state income taxes withheld from the conversion. Again, that simply passes the tax obligation to a different bucket. In most cases, you will want to pay the taxes out of a non-retirement account if you have the means to do so.

Additionally, I elected not to have Vanguard send me a Tax Withholding Notice. I’m aware of the conversion I am making, and having them send me a form in the mail doesn’t do me any good. It’s a waste of time, money, and resources. And Vanguard works hard to keep their investment management fees low and passing on savings to their members. So it’s in the best interest of all Vanguard members to choose electronic notices when possible.

Step 7. Confirm the Conversion

You will need to click the Continue button at the bottom of the Roth Conversion page (as seen in the screenshot above). The next screen will be the confirmation page. Simply review the information, then submit it. The conversion will be official, though it may take some time for the conversion to happen, especially if you have securities in your Traditional IRA that need to be closed out.

It’s also best to ensure there are no pending transfers, trades, or other actions within the account you are converting to a Roth IRA.

What Next?

You should be good to go and begin investing in mutual funds! You will likely see a pending transaction in both your Traditional IRA and Roth IRA accounts. It may take a day or three for the accounts to settle. That’s normal. Just verify everything goes through properly.

Also be sure to keep good notes of your actions. You will want to have records when you file your taxes the following year. My tax situation is fairly complex, due to running a small business, paying quarterly estimated taxes, participating in a small business retirement plan, doing back-door Roth IRAs, and similar fun things. So I keep a spreadsheet tracking all of my financial accounts, the dates I make contributions and the contribution amount, and anything other major financial transactions, such as this Roth IRA conversion.

This spreadsheet is part of a larger spreadsheet I keep to track my net worth, charitable contributions, and other financial activities.

Here is how to do a 401k rollover at Vanguard.