How to Buy a VA-Approved Condo

Purchasing a VA-approved condo can be challenging. This guide simplifies the process, ensuring you understand the steps involved in receiving VA condo approval.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

A condominium – condo, for short – is an individually owned, private unit within a community of other similar units. Condo owners own the interior walls of their property while jointly sharing the condo’s exterior with the community.

Military members, veterans, and surviving spouses of fallen service members can use the VA home loan program to finance a condo.

Condo ownership offers some advantages:

- Condo fees cover exterior maintenance and landscaping – one less thing for deployed military members to consider.

- Community condominium ownership means you’re always close to neighbors if you need help.

- Unlike rent for a similar property, condo mortgages qualify as a tax deduction.

The VA’s lender handbook, VA Pamphlet 26-7, details VA mortgages, including condo approval guidelines, eligibility, fees, and appraisals.

Key Takeaways:

- VA Loan Eligibility: Military members, veterans, and surviving spouses can use VA home loans to finance a condo, offering benefits like tax deductions on mortgages.

- VA Condo Approval Process: Check the VA’s approved condo list, and if your condo is not listed, work with a lender to apply for VA approval, though this process can take time.

- VA Condo Approval Requirements: Condos must meet specific VA criteria, including financial stability, sufficient owner-occupancy rates, and compliance with VA guidelines to ensure veteran protection.

- Common Reasons for Denial: Low owner-occupancy rates, financial instability, excessive commercial space, and restrictive bylaws can lead to a condo’s VA approval denial. However, veterans may be able to apply for a waiver if their request is rejected.

How do condos get added to this list?

Often, condo builders or developers will submit their properties for VA approval. This can be part of their marketing strategy to make the condos more attractive to potential buyers who are veterans or active servicemembers.

If the condo builder or developer doesn’t submit their properties, potential buyers can ask the developers or owners to do so.

How to Use the VA-Approved Condo List

If you’re interested in purchasing a condo with your VA loan benefit, the VA’s approved condo list is a great place to start to ensure the condo is eligible. To do so, follow the steps below.

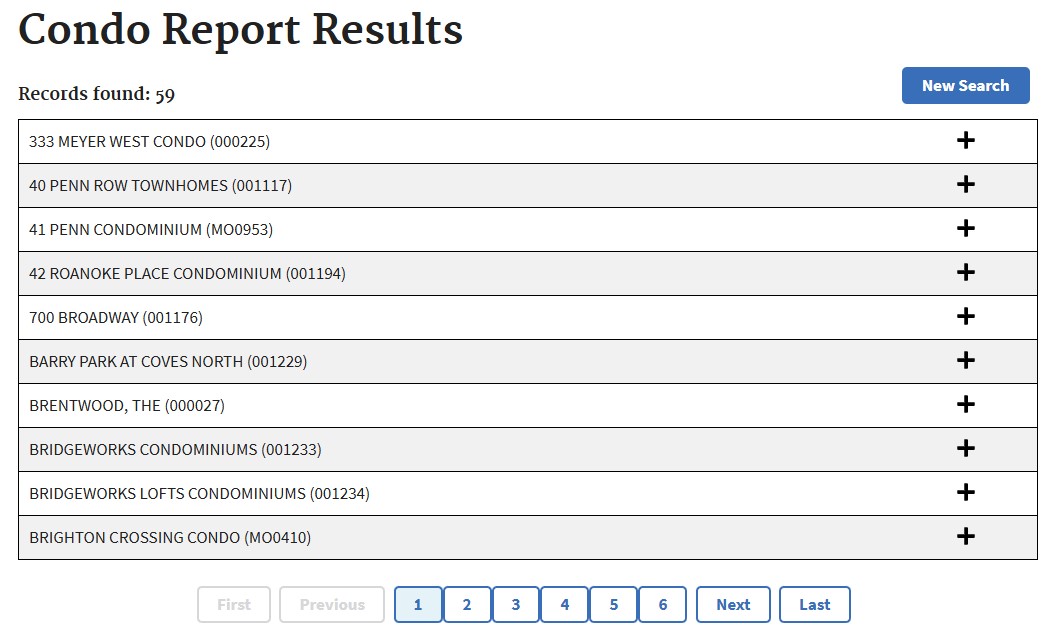

1. Check the VA’s easy-to-use approved condo list to find a VA-approved condo or determine if a condo is eligible for VA financing. To check this list, you’ll need some basic information. You can choose between the condo’s name, ID, regional office, or general location information like city and/or state.

As of July 2024, the list you get based on your search will look like this:

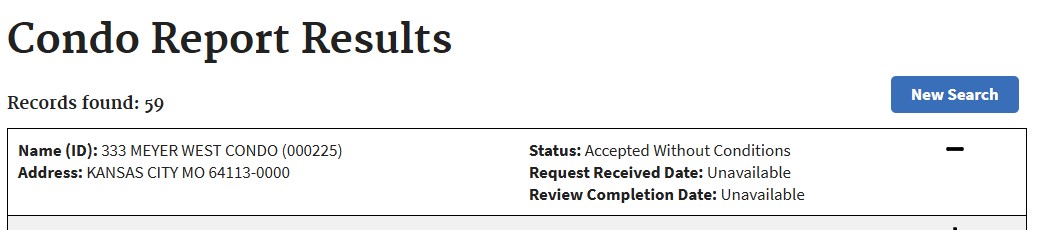

Click the plus icons to get more details on your desired condo.

Be sure to check out the “Status” field for your desired condo, because the list will return approved condos and rejected ones. So, just because you see your condo listed after your initial search doesn’t mean your condo is approved. In general, you’ll see one of the following statuses:

- Accepted Without Conditions: This status means that the VA has thoroughly reviewed the condo, and it meets all the necessary criteria without any additional conditions or requirements. It is fully approved and eligible for purchase with a VA loan.

- Conditionally Accepted: This status indicates that the condo project has been reviewed and meets most of the VA’s criteria. Still, some conditions must be met before full approval can be granted. These conditions might involve specific documentation, minor changes to the project, or other requirements that the condo association must fulfill.

- HUD Accepted: This status indicates that the condo project has been accepted based on its approval by the Department of Housing and Urban Development (HUD). The VA often accepts HUD-approved condos, recognizing that they meet similar standards required for VA approval.

- Rejected: This status means that the condo did not meet the VA’s approval criteria. The reasons for rejection can vary and may include issues related to the condo’s financial health, legal standing, or physical condition. A rejected status indicates that the property is not eligible for purchase with a VA loan.

- Withdrawn: This status means that the builder, developer, or submitter has withdrawn the application for VA approval. This can happen for various reasons, including changes in the condo project, financial issues, or a decision not to pursue VA approval.

- Suspended: A suspended status indicates that the condo’s approval is temporarily on hold. This can occur if the VA requires additional information or if unresolved issues need to be addressed before the review process can continue.

2. If you don’t see your condo on the VA’s list, find out if the Department of Housing and Urban Development (HUD) has already approved it. Projects with HUD or USDA approval may not need further review, according to the VA.

3. If the condominium isn’t on any government agency’s approved complex list, it may be because the condo developer or association has not yet applied to the VA for approval.

What to do next based on your condo’s status

Finding a condo with a VA-approved status of “Accepted without conditions” can simplify the buying process for veterans and servicemembers. However, if your desired condo has a different status, there are still steps you can take to potentially secure VA loan approval:

HUD Accepted

If the condo is HUD Accepted, it’s generally treated the same as if it were VA-approved. In this case, you should confirm with your lender that they accept HUD-approved condos for VA loans. Most VA lenders will process your loan as if the condo were fully VA-approved.

Conditionally Accepted

If the condo is Conditionally Accepted, you or the condo association will need to meet the conditions specified by the VA. This might involve providing additional documentation or making certain changes to the condo project. Work closely with the condo association and your lender to address these conditions. Condo associations are generally cooperative in working with potential buyers to resolve issues, as having VA approval can significantly increase the marketability of their units. Once the conditions are met, the condo can be fully approved, making it eligible for purchase with a VA loan.

Rejected

If the condo is Rejected, here’s what you can do next:

- Understand the Reasons: Request details on why the condo was rejected. Sometimes, issues can be minor or administrative and might be resolved with additional information or corrections.

- Address the Issues: Work with the condo association to address the reasons for rejection. The condo can be resubmitted for VA approval if the issues are resolved.

- Find Another Condo: If the issues are significant and cannot be easily resolved, you may need to consider other condos that are already VA-approved or have a more favorable status.

Withdrawn

If the condo’s status is Withdrawn, it means the approval process was halted by the submitter (builder, developer, or buyer). In this case:

- Ask About the Withdrawal: Find out why the application was withdrawn. Sometimes, the withdrawal might be temporary, or the issues leading to withdrawal might be addressable.

- Reinitiate the Process: If the condo association or builder is willing, they can reinitiate the VA approval process. Ensure all necessary information and documentation are provided.

Suspended

If the condo’s status is Suspended, it indicates a temporary hold on the approval process. Here’s what you can do:

- Get Details on Suspension: Understand the reasons behind the suspension. It might be due to missing information, legal issues, or other concerns.

- Work to Resolve Issues: Collaborate with the condo association and your lender to address the issues causing the suspension. Once resolved, the VA can resume the review process.

General Steps for Any Status

Regardless of the specific status, these general steps can help navigate the situation:

- Consult with Your Lender: Your lender can provide guidance on the specific steps needed to address the condo’s status and what options are available to you.

- Engage with the Condo Association: Work closely with the condo association or developer to understand and address the issues related to the condo’s approval status.

- Consider Other Properties: If resolving the issues proves too difficult or time-consuming, consider looking at other condos that are already fully VA-approved.

By understanding the status of your desired condo and taking proactive steps, you can improve your chances of securing a VA loan and purchasing the condo you want.

VA Condo Approval Requirements

The VA doesn’t publish its condo requirements. However, the Minimum Property Requirements (MPRs) play a large role in condo approval, along with additional criteria specific to condos. Some of the requirements may include:

- At least 70% of the units in a condo community must be sold or under contract at the time of any VA borrower’s loan application.

- The condo owner’s association (COA) must offer specific owner rights, such as the right to examine the association’s financial records.

- The COA may not impose a right of first refusal clause, which dictates who a condo owner can sell to and when. If a COA or homeowner’s association (HOA) has such a clause, it must waive it for VA borrowers.

Lenders may also have their own requirements separate from what the VA wants.

Why Would a Condo Not Be VA Approved?

Several common factors can lead to a condo’s denial, including:

Low Owner-Occupancy Rate: The percentage of units occupied by owners is below the VA’s required threshold, typically around 50%.

Financial Instability: The condo association may have financial issues, such as inadequate reserves, high delinquency rates on dues, or insufficient insurance coverage.

Inadequate Documentation: Failure to provide complete or accurate documentation, including bylaws, financial statements, and insurance details, during the application process.

Litigation Issues: The condo association is involved in significant litigation that could affect its financial stability or operation.

Commercial Space: The presence of too much commercial space within the condo project exceeds the VA’s allowable limits.

Property Condition: The overall condition does not meet VA safety, structural integrity, or habitability standards.

Non-Compliance with VA Guidelines: The condo project fails to meet other specific VA guidelines, such as restrictions on leasing, the rights of the condo association, or the ability to amend bylaws.

Occupancy Restrictions: The condo association imposes restrictions on who can purchase or occupy units that do not align with VA requirements.

Developer Control: The developer retains control over the association, which may pose a risk to the long-term stability of the project.

If a veteran’s condo request is rejected, they can apply for a waiver. By addressing the VA’s concerns and providing additional documentation, veterans can potentially overturn the initial decision and secure approval for their desired condo.

Buying a Condo with a VA Loan

The VA also requires specific documents before it will approve a loan, according to its lender handbook.

Required Documents May Include:

- Declaration of covenants, conditions, and restrictions

- HOA or COA bylaws

- HOA or COA articles of incorporation

- Plat, map, or air lot survey of the condo project and its units

- Condo development plan and schedule

- Existing and proposed HOA or COA budgets

- Minutes from HOA or COA meetings

- HOA management agreement

Your regional VA loan center will review and approve submitted documents during your loan underwriting process. Keep in mind that the VA or your lender may request additional documents.

Keep in touch with your real estate agent and VA loan underwriter to fulfill requirements quickly.

Frequently Asked Questions

How long does it take the VA to approve a condo?

The average VA condo approval time is 15-30 days, according to the VA. Once you get approved, you may be able to close on a property within three to four weeks.

How much does it cost to get a VA condo approval?

There are fees associated with the VA condo approval process. These fees cover the cost of the VA’s review and processing of the application. The exact amount can vary based on the complexity of the condo project and the region. Typically, the builder, developer, or condo association is responsible for these fees. However, in some cases, the cost might be passed on to the buyer or shared between the parties involved. It’s important for potential buyers to inquire about these fees upfront to understand who will bear the cost during the approval process.

More Reading

VA Loan Rates – Compare Today’s VA Home Loan Rates

Guide to VA Appraisal Fees and Process