Tax Benefits of Deployment: Combat Pay, Tax Filing Extensions and Much More

Military members who deploy are eligible for tax benefits, including tax-free combat pay, tax deadline extensions, tax-free TSP contributions and more.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

Expert Reviewed by: Mike Hunsberger, ChFC®, CFP®, CCFC

Serving in a combat zone is mentally, physically, and emotionally difficult for both servicemembers and their families. Fortunately, the military attempts to relieve some stress by offering tax advantages on military pay to servicemembers deployed to combat zones. With a few key tax deductions, your time in the field can be financially beneficial.

Key Takeaways

- Combat Zone pay is tax-free, substantially increasing take-home pay.

- Deployed servicemembers receive automatic benefits like extended filing deadlines and no penalties or interest during the extension period.

- Special savings opportunities, such as tax-free Roth IRA contributions, increased TSP limits, and the 10% interest Savings Deposit Program, can help build wealth quickly during deployments.

We’ve created your go-to guide to tax benefits and exclusions only available to those serving in combat zones, helping you navigate complex tax rules and maximize your financial benefits while serving your country.

Combat Zone Tax Exclusion (CTZE) Eligibility

The most impactful tax benefit for deployed servicemembers is the Combat Zone Tax Exclusion (CZTE). It allows military personnel serving in designated combat zones to exclude all or part of their military pay from federal income tax.

To be eligible for the CZTE, you must:

- Serve in an area designated by the President as a combat zone by Executive Order

- Serve in an area designated by the Department of Defense as a Qualified Hazardous Duty Area (QHDA)

- Be receiving Hostile Fire Pay or Imminent Danger Pay

You can also qualify if you have been hospitalized due to wounds, disease, or injury while serving in a combat zone. Combat zones currently include areas in the Middle East, Africa, and parts of Europe supporting Operation Inherent Resolve. The IRS regularly updates the list of qualifying locations; therefore, please check with your finance office or the IRS website for the most current information.

Tax Benefits for Deployed Soldiers

Antwyne DeLonde is an Army veteran who served in a combat zone during Operation Iraqi Freedom in 2003. He says the CZTE made a big impact on his finances.

“When I served in a combat zone, one of the few financial upsides was the Combat Zone Exclusion, which meant much of my pay was non-taxable,” DeLonde says. “For enlisted members and warrant officers, all earnings during time in a combat zone are excluded from gross income. For commissioned officers, there’s a cap based on the highest enlisted pay rate.”

For 2025, the exclusion amount is up to $10,983 per month, which includes the highest enlisted pay amount of $10,758 plus $225 for imminent danger pay. The CZTE includes several pay buckets. Let’s break down what’s eligible for this tax benefit.

Tax-Free Pay

When deployed to a qualifying combat zone, several types of military pay become exempt from federal income tax. To qualify for these exclusions, you must serve at least part of one day per month. For example, if you arrive at your duty station on March 31st, you may exclude all eligible pay for the month of March.

- Basic Pay: Enlisted personnel and warrant officers can exclude all basic pay earned in a combat zone. For officers, the exclusion is capped at the highest enlisted pay rate plus Hostile Fire/Imminent Danger Pay. For 2025, the exclusion amount is up to $10,758 per month.

- Hostile Fire/Imminent Danger Pay: This additional pay (currently $225 per month) is tax-free for enlisted and commissioned officers.

- Hardship Duty Pay: Pay received for serving in difficult or isolated conditions is excluded from taxable income when earned in a combat zone.

- Family Separation Allowance (FSA): The $250 monthly payment for being away from family during deployment is tax-free, whether the servicemember is in a combat zone or not.

- Per Diem: Daily meal allowances and incidental expenses in combat zones are not taxable.

- Reenlistment Bonuses: If you reenlist while in a combat zone, your bonus may be tax-free, potentially saving thousands of dollars.

- Awards and Special Pay: Many special pays and bonuses received in combat zones are tax-exempt.

If a servicemember is taken as a prisoner of war or is missing in action while in a combat zone, they will continue to receive tax-excluded income for the rest of their time in the armed forces.

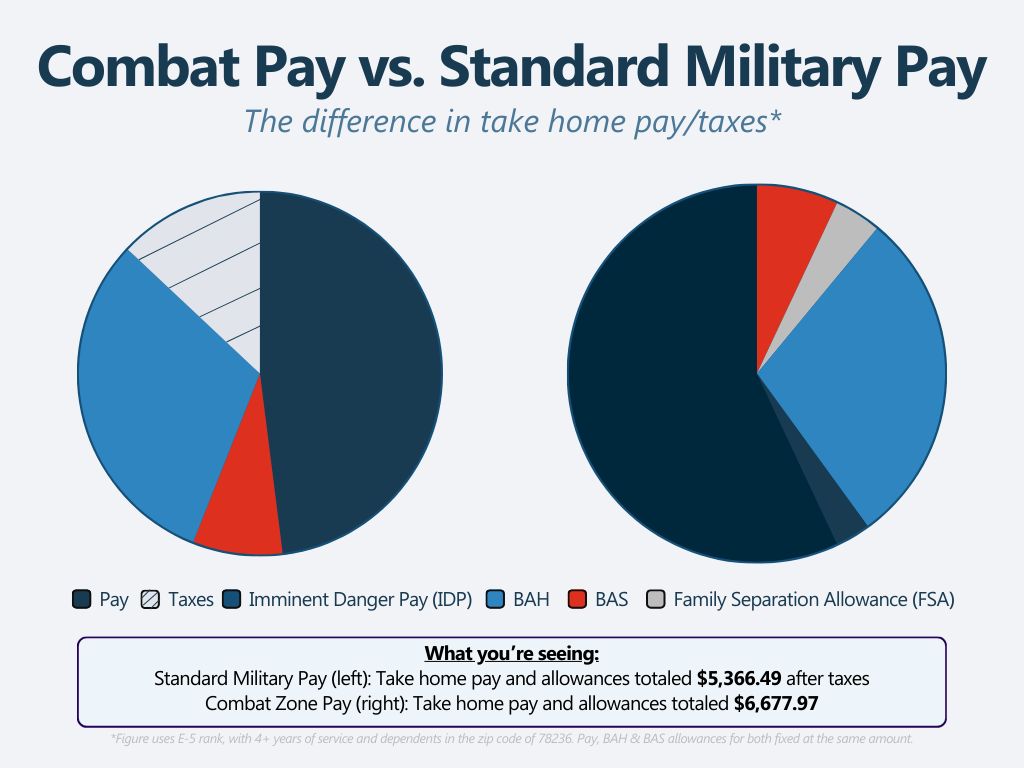

Example: Let’s compare the pay difference for a servicemember with an E-5 rank, 4+ years of service, with dependents living in San Antonio, TX. Military pay rates remain unchanged, along with BAH and BAS, as these are fixed rates. The difference arises when you add the tax-free component to the pay, along with the additional monthly payments for FSA and IDP.

The monthly pay breakdown roughly looks like this:

Standard Military Pay

$3,802.20 (Military Pay; E-5, 4+ YoS) + $1,935 (Basic Allowance for Housing) + $465.77 (Basic Allowance for Subsistence) – $836.48 (Federal Income Taxes)

=

Total take-home pay: $5,366.49

Combat Zone Pay

$3,802.20 (Military Pay; E-5, 4+ YoS) + $1,935 (Basic Allowance for Housing) + $465.77 (Basic Allowance for Subsistence) + $250.00 (Family Separation Allowance) + $225.00 (Imminent Danger Pay)

=

Total take-home pay: $6,677.97

As you can see, the difference in taxes alone is nearly $900 per month.

Tax Deadline Extensions

Tax filing season is also adjusted for servicemembers in combat zones. Kyle Harsha, owner of Money Matters Tax and Financial Services, points to some added leeway for their filing deadline.

“Military members who are in a combat zone automatically get an extension to file–they have 180 days,” Harsha says.

The deadline is also extended by the number of days that were left in the filing period when you entered the combat zone. For example, if you entered the combat zone on February 17th, you would have 180 days from when you leave the combat zone, as well as the 57 days that were left in your original filing period. This extension also applies to spouses filing jointly, even if they are not both deployed. During the extension period, no penalties or fees will accrue.

To request this extension, attach a statement to your tax return explaining your qualifying service or write “Combat Zone” on your paper return.

Earned Income Tax Credit (EITC)

Among the tax benefits available, some military families may qualify for the Earned Income Tax Credit (EITC), which can boost your tax refund if you’re a low- to middle-income earner. In some cases, higher-earning servicemembers who wouldn’t normally qualify may now be eligible because their income is reduced under the Combat Zone Tax Exclusion (CZTE).

If your income is too low to claim the full credit, you can choose to include your nontaxable combat pay as part of your earned income when calculating the EITC. Even though this pay isn’t taxed, adding it in can help you qualify or increase your refund.

Example: A servicemember with two children earning $20,000 in regular pay plus $15,000 in tax-free combat pay could choose to include the combat pay in their EITC calculation, potentially increasing their credit by several thousand dollars.

State Tax Benefits

Most states won’t tax your combat zone deployment pay. The primary reason is that states often model their tax structures after federal guidelines, then adjust them slightly to best suit the state’s needs. Since the federal government doesn’t tax your income, states don’t either.

Some states don’t collect any state taxes on military pay. If you’re a veteran/military retiree, then your retirement pay may not be taxed at all as well.

Note: Some states offer additional tax benefits, like Minnesota, which offers a bonus $120 per month (or partial month) if you’re deployed to a combat zone.

Check with your military tax professional to learn about your specific state benefits.

IRA Tax Benefits

Individual retirement accounts offer the ability to tack on extra retirement savings, but they are typically only available if you have taxable income. However, the Heroes Earned Retirement Opportunities (HERO) Act, passed in 2006, created an avenue for servicemembers to invest their combat pay in either a traditional or Roth IRA.

This law not only allows servicemembers to increase their retirement savings, but it also creates an opportunity for completely tax-free growth when using a Roth IRA. Roth IRAs are typically funded with after-tax income, and qualified withdrawals are made tax-free. When tax-free combat pay is contributed to a Roth IRA, the benefit is even greater—both the original contribution and all future investment growth can be withdrawn without owing taxes. Servicemembers may contribute up to the annual limit of $7,500 for 2026, or $8,600 if age 50 or older.

Tax-Exempt TSP Contributions

The Thrift Savings Plan (TSP) offers a tax-deferred investing option for all servicemembers, but there are a few benefits for those earning combat pay:

- TSPs are normally funded with taxed base pay, but those covered under the CZTE may contribute tax-free combat pay.

- The annual additional limit allows servicemembers to contribute up to $72,000 per year, which is much higher than the normal $24,500 limit. Maximizing TSP contributions during deployment periods can enable servicemembers to significantly boost their retirement accounts.

Deferred Payment Option

If you owe taxes and believe that your military service is why you can’t afford to pay them, you can apply to defer your tax bill until 180 days after you leave the military. During that time, the owed amount won’t be subject to interest.

Commissary and Exchange Privileges

While you’re serving, the military attempts to make life a little more affordable. Purchases at military commissaries and exchanges are always sales tax-free. Even if you’re deployed and separated from your family, they can access the commissaries and exchanges. They may also be eligible for special deployment discounts and programs for families of deployed personnel.

Tax Liability Forgiveness

Life in a combat zone is not without the ultimate risk. However, if a servicemember dies while deployed in a combat zone or from wounds received in a combat zone, the IRS will forgive all tax liability in the year of death as well as the previous year that ended on or after the first day of service in the combat zone.

Travel Expenses for Armed Forces Reservists

Although not all reservists will serve in a combat zone, the unreimbursed costs of their travel, lodging, and meals are not taxable if they are called more than 100 miles from their home base. These expenses are an “above-the-line” deduction, meaning you don’t need to itemize to claim them.

Filing Taxes While Deployed

If filing while deployed is burdensome, you can use your free 180-day extension, plus the length of your deployment. However, if your family back home is counting on a refund, these resources can help.

- Military OneSource: Offers free tax filing and consultation services through MilTax.

- Volunteer Income Tax Assistance (VITA): Albeit a less common practice, it provides free tax preparation on some military bases (may be limited to junior servicemembers)

- Power of Attorney: Consider giving a trusted family member power of attorney to handle tax matters while deployed.

- Electronic Filing: The most efficient method for deployed personnel, allowing quick submission and refunds.

Other Deployment Benefits

Beyond tax advantages, deployments offer additional financial benefits:

- Rest & Recuperation Leave: For long deployments, the military will pay for your travel to designated locations for the opportunity to recharge. You may combine your R&R leave with other types of leave when requested.

- Savings Deposit Program (SDP): Servicemembers in combat zones can deposit up to $10,000 with a guaranteed 10% return. This rate only accrues in the combat zone and for up to 90 days afterward.

- Family Separation Allowance: $250 monthly for deployments over 30 days. This benefit is intended to help defray the cost of childcare and other hardships caused by deployment.

- Hostile Fire/Imminent Danger Pay (IDP): Additional $225 monthly in qualifying. locations. (prorated to the actual days if just IDP)

Final Point

Leaving your family and home base for a combat zone can cause a great deal of stress, but they also offer the chance to maximize your pay. If you can afford to contribute more to your TSP or Roth IRA, your tax-free investments can prove very valuable.

If you’re unsure of how to proceed, connect with one of the military tax professionals. A tax professional familiar with military benefits will help you make the most of your combat zone perks.