Military Lending Act: Protecting Military Members from Predatory Lending

The Military Lending Act (MLA) is a legal protection that exists to protect servicemembers from predatory financial practices.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

The Military Lending Act Protects the Military Community

The Military Lending Act Protects the Military Community

How often do you read the fine print of contracts? What is the interest-rate cap for consumer loans for military members and their dependents?

Don’t feel bad if you aren’t confident with your answers to the questions above. That is exactly where the MLA comes in.

The Consumer Finance Protection Bureau (CPFB), an organization entirely dedicated to creating bright lines of clarity in lending, offers a host of information on fair practices and resources for consumers on lending in a general capacity. It is vital for all citizens to learn what allowances and limits are normal versus excessive. This resource is your starting line.

What is the Military Lending Act?

Essentially, the MLA ensures that service members and their dependents don’t fall victim to outrageous interest rates, charges or provisions associated with lending. A 36% annual interest cap military annual percentage rate (MAPR) is applied to the following:- Finance charges

- Credit insurance fees or premiums

- Participation, cancellation, application or other fees

- Add-on related products sold along with the credit within an agreed-upon contract

- Student loans

- Credit cards (as of 2017)

Who is Eligible for MLA?

Your local JAG office is the best place to go for advice, as well as to determine whether your personal situation falls under the ark of coverage. Active duty is generally the key phrase to look for when determining coverage. The following members are eligible for protections under the MLA:- Active-duty members

- Active-duty Reserve, National Guard troops on Title 10 orders and AGR troops

- Dependents:

- Spouses

- Children under age 21

- Children up to age 23 if enrolled full-time in an institute of higher education or is incapable of self-support because of a mental or physical incapacity that occurs while a dependent of a service member

- Dependents earning over half-time support or those earning over half-time support with any mental or physical disability

- Same-sex couples of eligible members

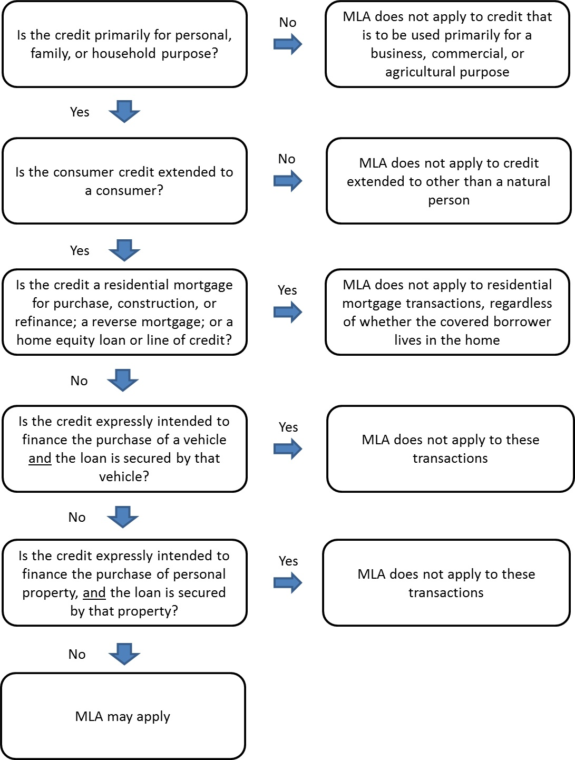

When Does the MLA Apply?

Unfortunately, the list of what is not covered is longer than what is. Lending situations expressly covered under the MLA include:- Payday loans – Short-term loans, generally less than $500, which are due upon the borrower’s next paycheck

- Deposit advance lending – Similar to payday loans, but made by financial institutions; the borrowed amount is automatically withdrawn from the borrower’s next paycheck

- Vehicle title loans – Short-term loan using the borrower’s vehicle as collateral

- Overdraft lines of credit – Lines of credit at a banking institution to prevent overdrawing the member’s checking account

- Installment loans – Unsecured loans that are repaid over time with fixed payments; generally personal loans

What Isn’t Covered

Eligibility under the MLA guidelines is perhaps one of the most important fine print outlines consumers need to read in full. The MLA does not cover loans that relate to the procurement of property, such as a home or car. Examples include:- Home mortgage loans

- Building loans for a home

- Home equity lines of credit or credit loans

- Personal property loans

- Auto loans

Additional Benefits Under the Military Lending Act

Though not expressly a benefit from the MLA, many credit card companies interpret the MLA in such a way as to waive annual credit card fees for military members and their qualifying dependents. These include major credit card issuers, such as Chase Bank and American Express, both of which waive annual credit card fees, even for some of their more popular travel cards. Some of those cards carry annual fees that would otherwise run several hundred dollars per year and provide similar value in benefits to cardholders each year. Some of the perks can include free airport lounge access, annual travel credits, excellent rewards on purchases and much more.