Comparing E7 Retirement Pay: Active-Duty Versus Reserve

Learning how to calculate your military retirement pay is essential for planning. This article compares active duty retirement pay and a Guard/Reserve retirement.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

Are you considering leaving active duty for the National Guard or Reserves? This article compares each type of retirement at the rank of E-7. Follow these steps and substitute your anticipated retirement rank to see how retirement compares between active duty and the Reserve Component.

Note: This article uses the E-7 pay grade and 2016 pay scales. However, the examples work the same using any pay grade and pay tables from any year. Just follow the steps and plug in your pay grade and current or anticipated pay to understand how to compare active duty retirement pay and Reserve Component retirement pay for the same pay grades.

Is reserve retirement the same as active duty service retirement

In several ways “yes” but there are also some significant differences you should know as well.

Reserve retirement uses the same broad principles as the Active Duty system, but instead of basing retirement pay on years of service, Reserve retirement is determined using Retirement Points. A qualifying year is a complete year in which a Soldier has earned a minimum of 50 retirement points.

Members who accumulate 20 or more years of qualifying service are eligible for reserve retirement when they reach age 60. In some cases, retirees may qualify at a younger age.

These are Final Pay Plan and High-36 Month Average Plan are the two non-disability retirement plans currently in effect for qualified reservists.

The Final Pay Plan uses a multiplier percentage that is 2.5% times the years of creditable service. The creditable years of service is determined by the sum of all accumulated reserve points divided by 360. The High-36 retirement plan is the total amount of monthly basic pay the member was entitled to during the member’s high-36 months divided by 36.

By contrast, active duty retirement is calculated using the REDUX Plan (available only to active duty members who entered service on or after August 1, 1986), the Final Pay Plan or the High-36 Month Average Plan. Active duty members must also have a minimum of 20 years of creditable service but the big difference is that they can apply for retirement at the end of their career instead of waiting until age 60.

How do I calculate my military retirement pay? What is the average Reserve retirement pay?

The Department of Defense uses a multi-step formula to compute retirement pay, so there is no definitive answer when it comes to what the average Reserve retirement pay is.

A better way to address this question is to look closer at what those steps are and then use your circumstances to come up with a dollar amount that is applicable to you.

The Retired Pay Formula is determined by multiplying your retired pay base by a service percentage:

Retired Pay Base x Service Percent Multiplier = Gross Retired Pay

Gross retired pay is rounded down to the nearest dollar.

Each year of active duty service is worth 2.5% toward your service percent multiplier. So the longer you stay on active duty, the higher your retirement pay. For example, a retiree with 20 years of service would receive 50% of their base pay (20 years x 2.5%).

A retired reserve member converts points to active service equivalents by dividing those points by 360. For example, 7200 retirement points divided by 360 = 20 years of active duty service (2.5% x 20 years = 50%).

For disability retirements, you would receive 2.5% for each year of service, or a disability percentage assigned by the service at the time you retire. In either case, the multiplier is limited to 75 percent by law.

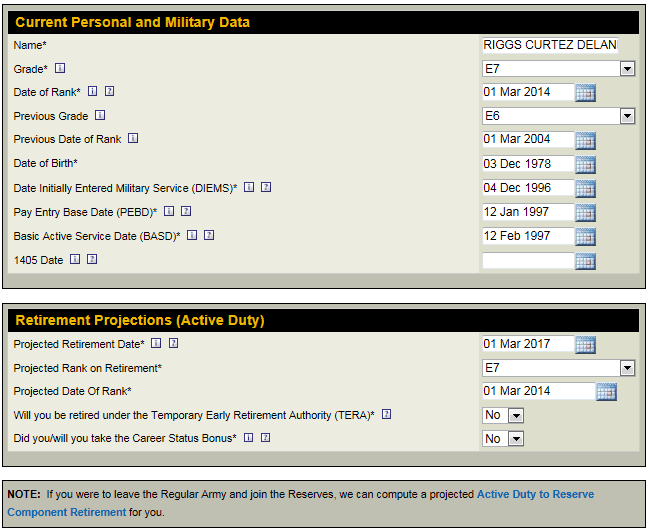

Examples of E7 Retirement Pay

Consider two 18-year-olds who join the military on the same day.

The first stays on active duty for 20 full years to retire as an E-7. They’ll base their pension on 2.5% x 20 years = 50% of their High-Three retirement system. Under the current High-Three* rules, their pension would be 50% of the average of the highest 36 months of base pay.

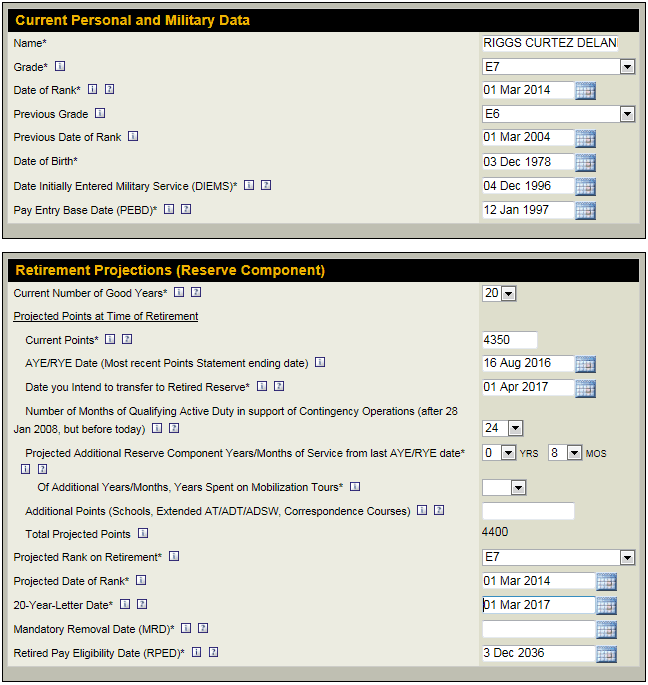

The second 18-year-old serves eight years on active duty while advancing to the E-6 pay grade, and then separates for a Reserve billet. Over the next 12 years as a drilling Reservist, they complete their “weekend a month, two weeks a year” of drills and active duty, while also mobilizing for two separate year-long deployments.

They get promoted to E-7 at about the same career point as their active-duty counterpart. Upon reaching 20 years of total service (eight years of active duty plus 12 “good years”) they request retirement awaiting pay.

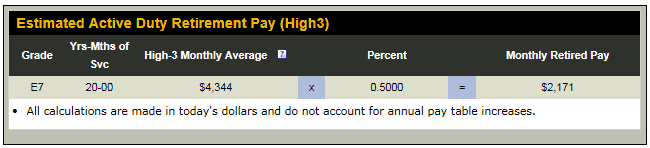

Both E-7s are the same age, the same rank, and subject to the High-Three rules. However, the active-duty E-7 retires and immediately starts drawing a pension. If they retired in 2016 then this calculator sets their pension at $2,171.00/month or $26,052.00/year.

Their pension includes annual cost-of-living adjustments that are roughly equivalent to the Consumer Price Index, the government’s official measurement of inflation. These COLAs will continue for as long as they (and their survivors, if they chose a survivor benefit plan) draw their pension.

How To Calculate An E7 Reserve Points

When the second service member joined the Reserves, their active-duty time was credited to their Reserve point count at the rate of one point for each day. Each year-long mobilization would earn at least another 365 points.

By serving “a weekend a month, two weeks a year” over their other 10 “good years”, they can conservatively be expected to average another 75 points each year. These are average numbers, some Reservists will earn more points, some will earn less.

At retirement, the Reservist would have a point count of eight years of active duty, 10 years of drills, and two one-year mobilization periods.

Their total would be at least, 8×365 + 10×75 + 2×365 = 4400 points.

- 8 x 365 (Active Duty) = 2,920

- 10 x 75 (Drills) = 750

- 2 x 365 (Deployments) = 730

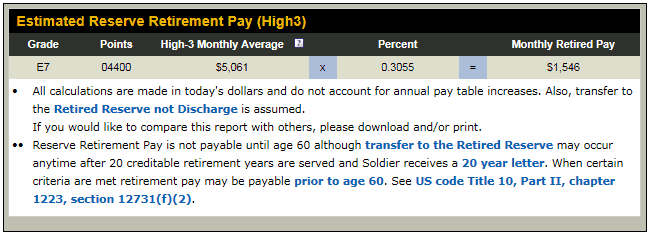

If they retired in 2016, this calculator sets their pension at $1,546.00/month or $18,552.00/year. Of course, pay wouldn’t begin until age 60.

The current instruction convert points to equivalent years by dividing into 360 (not 365). The percentage earned toward a Reserve pension would be 2.5% times the point count divided by 360, or 30.5%.

Although they were mobilized for two of their 12 years in the Reserves, at this point the Reserve E-7’s pension eligibility is only about 60% (30.5%/50%) of the active-duty E-7’s pension.

Click here to calculate a reserve retirement.

The Reservist’s pension also doesn’t start until they’re age 60– another 22 years. The good news is that because they “retired awaiting pay” instead of “resigning” from the Reserves, their pension will be calculated using the E-7 pay scale and maximum E-7 longevity in effect at age 60.

Pay Changes

It’s very difficult to predict how E-7 pay will change over the next 22 years, but it would be nice to have some numbers to refer to before making a decision to stay on active duty or to transfer to the Reserves. One pay assumption would be that it would keep pace with the civilian equivalent of their E-7 specialty.

In that case, the military’s E-7 base pay scale would rise by roughly the Employment Cost Index. Hopefully, in 22 years, Congress and the Department of Defense will agree that an E-7’s salary should have about the same purchasing power that it has today. In that case, the ECI would roughly keep pace with inflation and the Consumer Price Index.

The reality is that it’s impossible to confidently predict future pay scales, the ECI, the CPI, or pension COLAs. However, since the all-volunteer force began in 1973, the only proven way to retain servicemembers has been to keep military pay competitive with its civilian equivalent. (Otherwise, we wouldn’t have volunteered)!

Congress has attempted for several years to raise military pay at the same rate as the ECI (even greater for some ranks) and the pension COLA calculation closely tracks the CPI. Despite the uncertainties of predicting the next 22 years of pay raises and pension COLAs, it’s reasonable to assume that future E-7 pay will have roughly the same purchasing power as today’s pay.

While awaiting retirement pay for those 22 years, the Reservist will also be credited with the maximum longevity in that E-7 pay grade– 26 years– even though they only served for 20 years. In the 2016 military pay tables, the pay for E-7>26 is over 13% higher than E-7>20.

So although the Reservist’s pension eligibility only had about 60% of the equivalent active-duty pension when they retired awaiting pay, by the time they’re drawing that retired pay their longevity pay scale has risen another 13%.

The result is that by age 60 the amount of the Reserve E-7 pension has risen to nearly 70% ([30.5% x (1+13%)]/50%) of the active-duty E-7’s pension. If all of the pay assumptions are reasonably correct (and that’s a mighty significant “if”), then in today’s dollars they’d receive approximately $1850/month or $22,200/year.

Now that we’ve gone through the calculations the hard way, you could build your own spreadsheet to tinker with various ECIs and CPIs.

Difference Between Active Duty & Reserve

The biggest difference between active-duty and Reserve pensions is that the active-duty E-7 immediately started drawing their pension at age 38 at 50% of their High-Three pay average in effect at retirement.

The Reserve E-7 would have also retired at age 38 but had to wait 22 years for their pension, calculated at the maximum longevity and pay table in effect during the year they turned 60.

If their pension at age 60 preserved its purchasing power at least as well as the active-duty E-7’s pension, then their first pension payment would be almost 70% of the active-duty E-7’s pension payment– even though the active-duty E-7 has been receiving a pension for over two decades.

When the 60-year-old Reserve E-7 finally starts drawing their pension, that income stream will continue to rise with the same annual COLA as the active-duty E-7’s pension. Their pensions will be one component of a retirement made up of tax-deferred accounts, taxable accounts, and any pensions from other (civilian or civil-service) careers.

The next post will show how to plan a retirement with multiple streams of income.

[*A couple of final notes for the expert reader: we could make this post a lot more complicated by having these E-7s choose the REDUX retirement plan, but I’m saving that analysis for a separate post. For now, let’s just say “Don’t do it.”]

[** This post assumes that the Reservist’s deployments did not make them eligible for an earlier retirement. Under current legislation, if those deployments had happened in 2008 or later then they may have been eligible to start receiving their pension as early as age 58. Learn more about early retirement from Guard or Reserves.]

Military Guide to Financial Independence

- Military pension

- TSP

- Tricare Health System

- & More