Term Life Insurance Vs. Survivor Benefit Plan (SBP) Side-By-Side Comparison

The stakes are high when choosing SBP. If you make the wrong decision, you’re stuck with it for life. Still, there are valid reasons to choose it. Which is better for you: SBP or term life insurance?

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

I’ve written several articles about the Survivor Benefit Plan (SBP). Each article received some unanticipated pushback from different sides. I recommend reading several viewpoints on the SBP so you can formulate your own opinion based on your personal situation.

This article is also the basis for a chapter for an ebook, Guide to the Survivor Benefit Plan, currently available on Amazon.

Do I Recommend SBP or Term Life?

I once wrote an article on the Survivor Benefit Plan (SBP) for a well-known military financial site. It drew criticism from several fee-only financial planners who argued that SBP is costly compared to other options. In fact, they recommended avoiding it altogether. But then I wrote another article on the benefits of term life insurance. That too sparked backlash. I guess you can’t please everyone.

SBP is valuable in certain cases, though term life insurance often makes more sense. I have no financial stake in either option; my analysis is based solely on individual circumstances. Here’s my analysis.

There’s No ‘One-Size-Fits-All’

Each situation is different.

Your situation is not exactly like anyone else’s, so you need to educate yourself and form your best opinion. Do the analysis or have it done for you..

Despite arguments on both sides, no one can prescribe a “one-size-fits-all” solution that is best for everyone.

Rules of thumb:

- SBP could be better when you expect your spouse to outlive you by 20, 30, 40 years or more.

- Term life insurance could be better when you expect to build adequate assets by retirement age, but need protection if you die before that.

There are many situations where SBP may not adequately address a financial need, or is a more expensive alternative to term life insurance.

That’s why SBP may not be a good choice for female service members. Women are statistically likely to outlive their male spouses. Unless there’s a significant age difference, it just doesn’t make sense. It might not be the best use of money for people who are otherwise financially stable and don’t need to rely upon a pension because their post-military career and choices have more than made up for it.

However, there are also situations where SBP makes perfect sense: an older male with a much younger female spouse may benefit from SBP for a very LONG time (at least she will…). For example, my grandmother outlived my grandfather for 30 years (she was 2 years older) and received SBP the whole time. So, for a male service member marrying a second wife who is 10 years younger, this makes perfect sense, since she’ll likely benefit for 40 years or more.

SBP also makes sense if there are health-related insurability concerns that can make term insurance unaffordable, or even unattainable. Also, if you outlive a 30-year term policy, you get nothing. Conversely, SBP is guaranteed for life. If you choose a life insurance policy over SBP, you need to take this into account. There are also situations where the decision isn’t so clear. For example, many people feel they may be on the right track toward retirement. Perhaps the retirement plan includes having that inflation-adjusted pension, retirement assets, and social security. However, what happens if you’re in your 40s or 50s (prime earning years with the highest living expenses for most people), and something disastrous happens? Your beneficiary might receive a guaranteed pension…but that doesn’t replace the expected income or the assets you expected to accumulate over time. Nor can you expect it to cover living costs while paying a mortgage and supporting kids at home.

SBP vs Term Life Side-By-Side Comparison

| Feature | SBP (Survivor Benefit Plan) | Private Term Life Insurance |

| Type | Pension continuation (monthly income) | Lump-sum life insurance payout |

| Purpose | Provide lifelong income to spouse/beneficiary | Provide tax-free cash to heirs after death |

| Payout Format | Monthly payments (up to 55% of retired pay) | One-time, tax-free lump sum |

| Coverage Duration | Lifetime (for spouse); until age limit for children | Fixed term (10, 20, or 30 years typically) |

| Cost | ~6.5% of retired pay (deducted monthly; pre-tax) | Varies widely; generally lower for healthy individuals |

| Health Requirements | None | Usually requires medical underwriting |

| Portability | Not portable (tied to the military retirement system) | Fully portable |

| Tax Treatment | Benefits taxable to the beneficiary | Payout is tax-free |

| Inflation Protection | Yes – Cost-of-Living Adjustments (COLA) | No automatic inflation adjustment |

| Flexibility | Irrevocable in most cases after the election | Highly flexible: can cancel, convert, or renew |

| Customizability | Very limited (few choices on structure and amount) | Highly customizable: choose term, amount, riders, etc. |

| Common Use Case | Lifetime financial security for the surviving spouse | Cover mortgage, education, or income replacement for dependents |

Which Would I Choose? Term Life or SBP?

While this doesn’t reflect everyone’s situation, I think it’s a pretty common one. In fact, it’s my personal situation. I’m a 40-year-old, soon-to-be military retiree in decent (but not Ironman) health.

My family has 3 children, a mortgage, one car payment (very low interest), and a couple of small student loans (less than $10K total). My wife is 1 year older than I, and my children are in elementary school, with two dogs, two canaries, and a lizard (uromastyx, if you’re interested). In other words, nothing unusual, and probably a situation a lot of people can identify with.

Identifying Insurable Financial Needs

Let’s start by identifying my financial need. My number one concern is the financial risk to my family if I die in the first 20 years after my military retirement.

Why 20 years?

After age 60+, I expect to have accumulated enough assets for my wife to pay her living expenses and provide for herself after I die, even without my military pension. We will have paid off our house and possibly even downsized, and our children will have long since been gone, so her living expenses will be much lower. Before that point, though, my wife will be looking at having to handle our pre-retirement expenses, and my plan needs to address that.

In my situation, I could either obtain SBP or a term insurance policy. My SBP would protect approximately $4,000 in monthly income (providing a $2,200 monthly payout, with annual COLA increases) for about $260. Since this is pre-tax money, that comes to about $195 per month after taxes. For that $195, I’ve been able to get underwriting on a 30-year, $1.5 million insurance policy.

I’m using a 30-year policy as a ‘just-in-case.’ I believe that 20 years would be sufficient to reach our financial goals, but I’m willing to purchase a 30-year policy to eliminate any doubt. We will compare the SBP payout (55% of $4,000, or $2,200 per month) to the cash flow from a $1.5 million payout.

Remember that peace of mind should be your number one priority. If SBP is your answer & nothing will change your mind, do not read further. However, this article attempts to compare SBP with another option that might better address your situation.

There are many assumptions, so please read them at the end of the article if you’re interested. If not, just know that I work on these scenarios a lot and am a Certified Financial Planner™. If anything, my assumptions are more conservative than they need to be. Caveats out of the way, let’s get to work comparing the two scenarios.

Break-Even: Using a side-by-side comparison of the payout numbers allows us to analyze the ‘break-even’ point…at what point does the COLA-adjusted SBP pension become a better financial option than a lump sum payout? The break-even point is defined as the year in which the invested lump sum, which replicates the SBP payout, is depleted. After the break-even point, SBP is the better option. Any shorter, and the term insurance is more attractive. To clarify:

- AFTER Break-even: SBP wins

- BEFORE Break-even: Term Insurance wins

Returns: We will adjust the COLA for SBP and hypothetical investment returns for the payout. These hypothetical investment returns are very low. In fact, the highest rate, 4%, is a generally accepted distribution rate in the financial planning industry that still allows for the long-term preservation of capital.

Calculating distribution: Instead of just assuming a 4% distribution rate, we’re comparing the guaranteed $2,200 monthly pension (adjusted annually for cost of living allowance increases), to how long a $1.5 million policy would last, if set aside and used to match the after-tax SBP payout. For example, at a 4% annual COLA adjustment, the $26,400 in Year One will become $27,456 in Year Two. After tax, this becomes $19,800 and $20,592, respectively. The distribution from the lump-sum investment will match this, first with earnings, then with principal. The calculations reflect the tax impact from earnings, but zero taxation on principal.

For the illustrations in this article, I’ve used a 40-year time horizon. At the bottom of each illustration is a bullet point summary of how much money you would have at the end of this period, as well as the SBP break-even point.

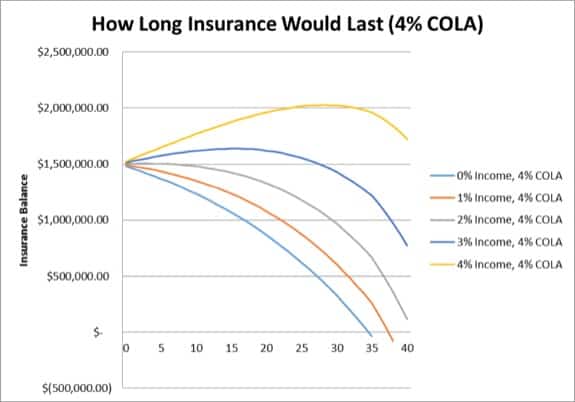

Illustration 1 – Break-Even Point

Illustration 1 represents the break-even point with an annual COLA adjustment of 4%. Most financial planners use 3-4 percent as an inflation assumption when preparing financial plans. Even though core PCE inflation hit 5% in 2022, those levels eventually dropped, and the inflation rate in early 2025 has been at or below 3%. So 4% is a conservative estimate.

Even with a 4% COLA, a $1.5 million portfolio lasts 30 years in all situations. The SBP break-even point is at least 35 years for any of these scenarios. Even if you took the money and put it under a mattress, you would be able to match the SBP payout for 35 years. And at a 4% income, you end up with more money than you started with at the end of 40 years!

| Numbers below: | Amount after 40 years | Breakeven Point |

|---|---|---|

| 0% Income | $ 0 Run out of money at 35 year mark | 35 |

| 1% Income | $ 0 Run out of money at 38 year mark | 38 |

| 2% Income | $114,437.54 | 40 |

| 3% Income | $772,879.56 | 45 |

| 4% Income | $ 1,725,825.83 | 53 |

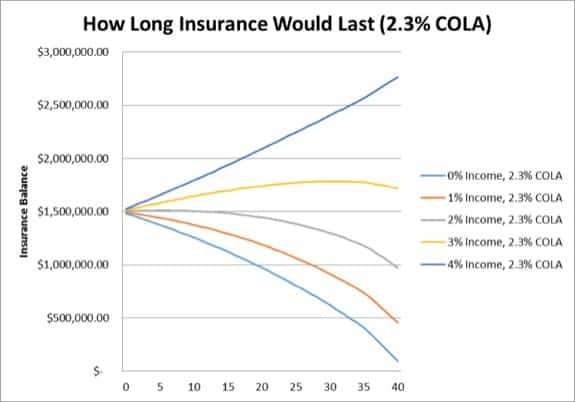

Illustration 2 – Smaller COLA

Illustration 2 is calculated the same way as Illustration 1, but with a COLA adjustment of 2.3%, which is a reasonable estimate based on adjustments over time.

In this illustration, you can see that every payout scenario lasts at least 40 years. Again, even if all you do is dole out money from under your mattress to match what you’d have received from SBP, you’d still have money left over at the end of the scenario.

| Numbers below: | Amount after 40 years | Breakeven Point |

|---|---|---|

| 0% Income | $95,576.94 | 41 |

| 1% Income | $453168.59 | 46 |

| 2% Income | $972,722.41 | 54 |

| 3% Income | $1,715,799.71 | 68 |

| 4% Income | $1,725,825.83 | 108 |

Will You Need Lots of Cash Immediately After Death? Think Twice about SBP

As an example, let’s imagine my wife used $500,000 for whatever she needed and had $1,000,000 set aside to cover her annual income. In the worst-case scenario (4% annual COLA, which she matches under the mattress money), that $1,000,000 would still be able to match the SBP payout through year 27. Instead of 108 years, $1,000,000 would get her through Year 57 under the 4% income, 2.3% COLA scenario. In addition to providing a steady income, an insurance policy gives you the flexibility to address immediate needs…SBP cannot offer this.

Although these projections seem outlandish, they may not be, as longevity increases keep pushing the boundaries of our life expectancies. There are plausible scenarios in which my wife could outlive me by 50-60 years and need income into her 100s. However, that scenario is not as much of a concern to me as the liquidity and immediate cash flow concerns.

Conclusion

In this scenario, a term insurance policy seems to be a more financially sound option than SBP.

However, if I predecease my wife by 30 years or more, she might be better off with SBP. With that said, 30 years gives her plenty of time to take control of her life after my demise, and to find the help she needs to move forward with her financial life.

Again, this article does not seek to persuade you into one decision or another. However, it does aim to show you an expanded definition of peace of mind. In my situation, peace of mind comes from the fact that:

Once my term policy expires, my wife and I have reached the point that she won’t need either it or SBP anymore in case I die.

Selecting a term life insurance policy is a more cost-effective way to replicate the SBP payout

The liquidity that a term life insurance policy provides so that my wife can get through those first few years after I die.

For more in-depth reading, you can check out the book I wrote, Guide to the Survivor Benefit Plan.

Methodology

- If even the thought of some investment risk (even US Government-backed securities or bank CDs) scares you, stop. While this discussion goes into scenarios with very low, achievable investment returns, which can be reasonably achieved with very safe investments, such as a treasury bond ladder or CDs, nothing is ever guaranteed.

- This article assumes fairly low COLA (inflation) rates. Since 2022, inflation rates have picked up but appear to be stabilizing. The assumptions are generally in line with inflation rates used by financial planners.

- This article ONLY addresses the cash flow issues that happen when there is a sudden loss of income before there are enough retirement assets to support living expenses. For this example, I’m primarily concerned about my wife raising our 3 children and paying the mortgage if I die in my 40s. I’m not as concerned about cash flow needs in our 70s. By the time we reach retirement age, our plan is to have enough retirement assets so that she does not have to rely on my pension (or SBP payout) to cover her living expenses. In this case, term insurance provides protection against a defined insurable need: the sudden cessation of pension income while you’re still building your retirement assets.

- This article doesn’t try to compare whether SBP is cheaper than insurance. I’m using information from my previous article, where I outlined how much insurance I would be able to purchase with the amount of money I’d otherwise use for SBP. You may find that you can buy more or less insurance, based on your particular situation.

- This article does not attempt to compare the amount invested in SBP vs. the amount invested in the insurance policy. It assumes that the same premium would purchase either the guaranteed SBP payout or a certain amount of life insurance. In this case, the comparison is between the SBP coverage of a $4,000 pension (which is $2,200 per month), or a $1.5 million payout. Your situation may allow for a lower or higher payout. Whether you die at Year 1 or at Year 29, you will have paid approximately the same amount for either outcome.

- This situation assumes that at the end of a 30-year term policy, you will have enough retirement assets to offset your SBP benefit. If you’re not comfortable with the fact that in Year 31, your pension could go to zero, stop. Choosing the Survivor Benefit Plan is better for your risk tolerance.

- There are worse things than outliving a 30-year term policy. However, you might be concerned about the thought of getting nothing for that money. Look at it this way: it’s the exact same result as if the service member outlives their spouse…you keep your WHOLE pension. In the meantime, the insurance policy protected you against the downside risk of losing your post-military earnings.

- This article assumes your insurable need is for a 30-year term policy. You may find lower rates (or a higher insurance policy for approximately the same premium) if you’re willing to accept a 20-year term, which some people may be willing to do if they are older and/or closer to financial independence.

- This article assumes that SBP proceeds are 100% taxable, while the insurance payout is not. However, earnings on the principal are taxable. We will assume the 25% tax rate on earnings from the life insurance payout.

- This article does not assume any special needs or situations beyond what I explained above. If your situation is significantly different from the one outlined above, you may have to do your own analysis to figure out what is right for you. In fact, you should analyze your own personal situation. It is YOUR life, and you need to OWN your decisions.