2026 COLA Military Rates

The Social Security Administration announced the 2026 Cost of Living Adjustment will increase by 2.8%. COLA impacts the everyday lives of military members because it is factored into numerous veteran benefits including military retirement pay, basic pay, VA disability pay and more.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

Cost of Living Adjustments (COLA) affect Social Security, retirement pay and veterans benefits like Department of Veterans Affairs disability compensation, annual military-base-pay cost-of-living increases, and location-based cost-of-living increases.

COLA is an acronym for cost-of-living-adjustment, which is an increase applied to certain types of income to help combat inflation. In 2026, the Social Security Administration (SSA) announced a 2.8% COLA increase, based on inflation-related data from the U.S. Department of Labor.

The military community is particularly affected each year when COLA rates increase. In particular, it’s vital for those living off their military retirement plans, veterans living with a disability they suffered during their time serving, or service members receiving monthly allowances for food.

How COLA Rates Affect Military Programs

COLA is pivotal to the lives of service members and veterans because of its role in:

- VA Disability Pay

- Social Security Payments

- Basic Allowance for Subsistence (BAS)

- CONUS and OCONUS COLA (Location-based adjustments for particular areas with a higher cost of living)

- Military Survivor Benefit Plan

Essentially, COLA increases ensure the money you may receive on a fixed pay rate still holds spending power for daily goods and services.

Your location impacts COLA rates. Continental U.S. cost of living adjustment (CONUS COLA) is a taxable benefit added to military pay to offset higher living costs in certain U.S. areas. This adjustment applies when local costs exceed the national average by 8% or more. This affects about 54,000 service members in 21 military housing areas.

If you’re stationed in Alaska, Hawaii, or abroad, you’ll likely receive the Outside Continental U.S. cost of living adjustment (OCONUS COLA). This non-taxable supplement depends on your rank, years of service, and number of dependents. OCONUS COLA accounts for higher living costs and exchange rates in foreign regions.

Federal law ties veterans’ benefits to COLA increases, however, Congress must pass a new version of the Veterans’ Compensation Cost-of-Living Adjustment Act each year.

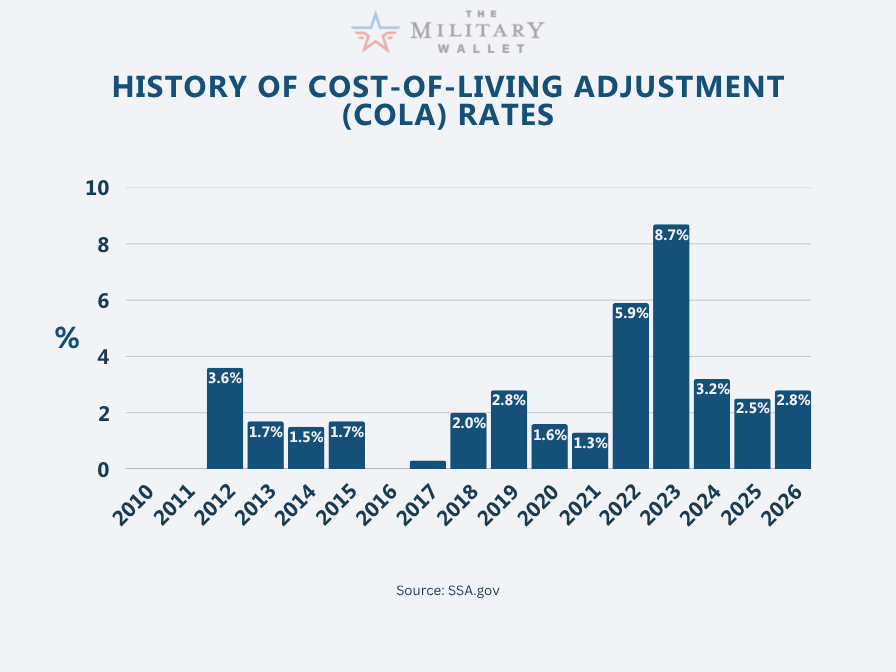

Historical COLA Rates for Military Retirement Pay

Cost of living adjustment rates vary each year, given the change in inflation. Below is a historical record of military retirement COLA pay raises:

Annual COLA increases are larger in years with higher inflation. Conversely, there was no COLA increase in 2010, 2011, or 2016 because of low inflation.

Note: While COLA affects things like VA disability pay, Military retirement pay, etc. It does not impact Military Pay and Drill Pay for Reserves/National Guard. Congress determines the rate of pay increase for service members each year in the National Defense Authorization Act, which serves as the Defense Department’s spending bill.

How to Calculate COLA Increases

The Department of Labor’s Bureau of Labor Statistics surveys over 80,000 goods and services to determine the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

Increases in costs for goods and services will result in a COLA increase for the following year. If there is no change or decrease in the cost of goods and services, there is no increase in the COLA. However, price decreases don’t decrease COLA-based benefits.

The Social Security Administration’s COLA rates act as a math equation each year. To apply the COLA adjustment, multiply the COLA rate percentage by what you earn or qualify for in the affected programs. Then, add that calculation to your current earnings or benefit to find the adjusted total.

For example, consider the 2.8% increase in 2026. If someone was making $500 in 2025, they would now make $514, because 2.8% of $500 is $14. So you would add $14 to the $500.

Stay Up to Date on Your Benefits

Join our free email newsletter for the latest updates on military benefits and expert tips for planning your retirement.