Military Service Members’ Guide to SCRA and MLA Credit Card Perks

Find out which credit cards offer the best military benefits under SCRA and MLA. See eligibility, benefits, and more for top cards like American Express, Chase, and more.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

Editorial Note: We may earn a commission through links from our partners. American Express is an advertiser on The Military Wallet. Commissions do not affect our editors’ opinions or evaluations. Terms Apply to American Express benefits and offers.

Under the Servicemembers Civil Relief Act (SCRA) and Military Lending Act (MLA), active-duty U.S. military members can receive several types of financial relief and protection, including annual fee waivers on premium credit cards.

Here is what you need to know.

What is the SCRA and MLA?

The Servicemembers Civil Relief Act (SCRA) provides legal and financial protections to members of the nation’s armed forces.

The SCRA is a law created to provide extra protections for service members in the event that legal or financial transactions adversely affect their rights during military service.

Several credit card protections are included, but service members can also take advantage of other SCRA benefits, including protection against default judgments in civil cases, home foreclosures, repossession of their property, and termination of residential housing and automobile leases without penalty.

The Military Lending Act (MLA) is a companion federal law that protects military members against certain lending practices. Under the MLA, creditors may not charge more than a 36% Military Annual Percentage Rate (MAPR) on a wide range of credit products. In addition to interest, the MAPR also includes costs associated with fees, charges for debt cancellation and suspension, and additional credit products, such as credit insurance. Lenders must disclose to you, orally and in writing, the MAPR that applies to the credit product you seek.

The MLA also requires no mandatory waivers of consumer protection laws. A creditor can’t require you to submit to mandatory arbitration or give up certain rights you have under state or federal laws, like the SCRA.

Creditors also can’t require you to create a military allotment, an automatic amount of money taken from your paycheck to pay back your loan. Also, they cannot charge a prepayment penalty if you repay part or all of your loan early.

Compare the rates, fees, and rewards of top credit cards for military servicemembers and veterans, including cards with waived annual fees under the SCRA, with our Card Finder tool powered by CardRatings.

SCRA and MLA Credit Card Benefits

Specifics will vary for each issuer, but in general, active duty service members may enjoy many of the following benefits:

- No annual fees

- No over limit

- No late payment fees

- No returned payment fees

- No fees for requesting copies of statements

- Waived or reduced credit card cash advance fees

- Cash back incentives

- Cash back programs for military-related expenses such as moving, uniforms, etc.

- No overseas transaction credit card fees

- Incentives for electronic payments or automatic electronic payment transfers

- Lower APR interest rates for military members, including many issuers who offer rates below those mandated by SCRA and MLA.

- Special perks or incentives for deployed service members or their dependents

- Special “reserve cards” for military families

Annual Percentage Rate (APR)

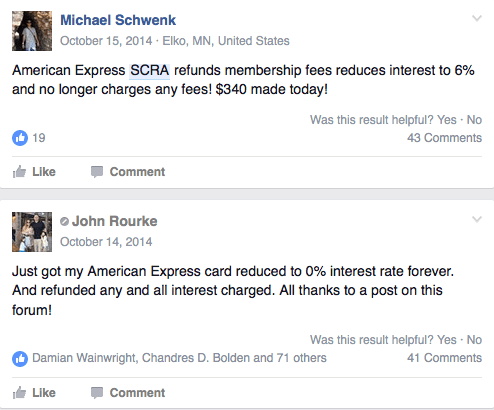

Under the SCRA, credit card rates are capped at 6%. Another important part of the credit card provisions is that most banks and credit card issuing companies will offer a refund on interest and annual fees for certain financial obligations incurred before a servicemember’s active duty military service. For example, if you bought a car or a boat with a 12% loan before serving, you can request to have your interest rate lowered to 6%.

The 6% cap applies to all debts incurred before entry into active-duty service, including student loans, credit cards, mortgages, and car loans. The cap remains in effect for the duration of a servicemember’s active-duty service.

Interest accrued above 6% must be forgiven, not just postponed, and the remaining monthly payments must be reduced to reflect the lower interest rate.

Eligible Branches of Service

All active duty members are covered by the SCRA, including those in the Army, Air Force, Coast Guard, Marine Corps, Navy, Space Force, Reserves, and National Guard. SCRA only applies to reservists and members of the National Guard when they’re serving on active duty orders over 30 days.

How to Access Benefits

To access SCRA benefits, servicemembers must apply to the lending institution where they are seeking the reduction.

Most types of consumer loans offered to active-duty servicemembers and their dependents must to comply with the MLA. These credit products generally include:

- Payday loans, deposit advance products, and vehicle title loans

- Overdraft lines of credit, but not traditional overdraft services

- Many types of installment loans, with some specific exceptions

MLA doesn’t cover credit that is secured by the property being purchased. That includes residential mortgages, mortgage refinances, home equity loans or lines of credit, or reverse mortgages. It also doesn’t cover loans on motor vehicles when the credit is secured by the motor vehicle you are buying or a loan to buy personal property when the credit is secured by the property you’re buying, such as for jewelry or a home appliance.

Determining if SCRA or MLA Benefits Apply to You

The military benefits you receive on credit cards depend on when you open a credit card account.

- SCRA benefits apply if you open an account before you are an active duty servicemember.

- MLA benefits apply if you open an account while you are on active duty.

If you apply for the credit card account while you are on active duty orders, or if you are a Guard or Reservist on 30-day or greater active orders or a dependent of an active duty service member, you are eligible for Military Lending Act (MLA) benefits while you are on active orders or a dependent of someone on active orders.

Qualifying for SCRA Benefits

If you apply for the account before your active duty orders, you are eligible for SCRA benefits while you are on active duty.

The SCRA applies to the following servicemembers:

- Active duty members of the Army, Marine Corps, Navy, Air Force, and Coast Guard;

- Members of the Reserve component when serving on active duty;

- Members of the National Guard component mobilized under federal orders for more than 30 consecutive days

- Active duty commissioned officers of the Public Health Service or the National Oceanic and Atmospheric Administration.

- SCRA rights may be exercised by anyone holding a valid power of attorney for the servicemember.

- Some SCRA protections also apply to dependents. SCRA benefits apply to spouses and children of qualified servicemembers and any person who relied on the servicemember for at least 50% of their support for up to 180 days prior to invoking SCRA benefits.

Qualifying for MLA Benefits

To qualify for MLA benefits, the credit account must be established while you or your active duty sponsor are on active duty orders lasting more than 30 days.

Borrowers covered under MLA are defined as:

- Active duty member of the Army, Navy, Marines, Air Force, Space Force, or Coast Guard

- Guard or Reservists on 30-day or greater active orders

- A spouse or child dependent of an Active Duty member of the Armed Forces as defined in 38 USC 101(4)

Major Credit Card Issuers and SCRA/MLA Benefits They Offer

While all card issuers must comply with SCRA and MLA laws, some credit card issuers go above and beyond laws on the books to support servicemembers and their families. Finding the right card depends on how you’ll use the card and what other benefits issuers offer for all users such as cash back categories, various promotions, and more.

Here are some of the biggest banks in the US and banks that specifically serve military members, and some of the SCRA/MLA benefits they offer servicemembers and their dependents.

The simplest way to check if you will receive MLA or SCRA protections on your account is to check the MLA Database or SCRA Database.

The MLA and SCRA database are the same databases that the credit card companies check to determine if you qualify for MLA or SCRA benefits.

If you are not listed as eligible in these databases, you will not receive MLA and SCRA benefits applied to your account.

You must be listed as eligible in these databases for the credit card companies to apply your military benefits.

American Express

American Express complies with all SCRA and MLA requirements.

The SCRA applies to Consumer, Small Business, and Corporate Card products and closed-end credit loan products. This even includes The Platinum Card from American Express and the American Express Gold Card, two of the best credit cards on the market. Eligible American Express customers will receive relief on accounts opened before the start of the servicemember’s active duty period, including credit cards and personal loans.

How to submit your request to American Express

Submitting your request online is the fastest way to request SCRA relief. You may also submit any relevant documents through the Document Center. This includes paperwork establishing active duty, such as documentation prepared exclusively by a branch of the military, the Department of Defense, or your commanding officer that indicates that you are on active duty (e.g., active duty orders, change of station orders, DD-214 forms, letters from commanding officers, etc.).

You can also the number on the back of your Card or 1-800-253-1720 to submit a request. If you are outside the United States, you can call collect at 1-336-393-1111. A third option is to send a copy of documents establishing your active duty status to: American Express, Attn: Servicemembers Civil Relief Act, PO Box 981535, El Paso, TX 79998-1535.

SCRA relief is available only on accounts opened prior to active military duty. For accounts opened while on active military duty, MLA coverage will be determined at the time of application, and those accounts will be ineligible for SCRA relief.

Please note that SCRA relief can only be requested online if the Card account for which you’re requesting relief is enrolled in American Express Online Services. If it is not, you may enroll your Card now.

American Express will advise you of your status up to 2 billing cycles after you submit your request.

The Platinum Card® from American Express

American Express offers one of the best money-saving perks to military servicemembers – it waives the annual fees for its credit cards, including on The Platinum Card® and the American Express® Gold Card.

With an annual fee of annual_fees and annual_fees, respectively, it’s easy to see how this under-the-radar perk can be a huge money saver for American Express cardholders, especially if you’re a service member who wants to enjoy the lucrative luxury perks that accompany The Platinum Card® from American Express, or the everyday practicality of the American Express® Gold Card.

Now that you know you can get your American Express annual fee waived as an active service member or spouse of a service member, what are some American Express cards to check out?

Learn more about our favorite below:

Armed Forces Bank

You will need to check with Armed Forces Bank to find out what SCRA and MLA benefits you qualify for when you have an account with that institution.

Contact the bank here.

Both the Visa Credit Card and the Credit Builder Secured Visa Credit Card from Armed Forces Bank do not carry annual fees, so the fee waivers under the SCRA and MLA are less impactful than those for some premium travel cards from other providers.

Bank of America

Bank of America complies with SCRA laws, including waiving fees and lowering your APR to 6% for all pre-service balances during active duty and for up to 180 days after separation.

Go here for more information to see if you’re eligible.

Learn more about all Bank of America SCRA policies on their FAQ page, or apply for benefits in several ways.

Phone:

877.345.0693 (outside the U.S., call collect: 817.245.4094)

Monday – Friday, 9 a.m. to 8 p.m.

Fax:

866.696.0292 (outside the U.S., fax collect: 302.525.5889)

Attn: Military Benefits Unit

Mail:

Military Benefits Unit

PO Box 673026

Dallas, TX 75267-3026

Overnight mail:

Military Benefits Unit

Department FL96000297

9000 Southside Blvd.

Jacksonville, FL 32256

Email:

Don’t send personal information via email unless it is sent through a secure method.

Barclays Bank

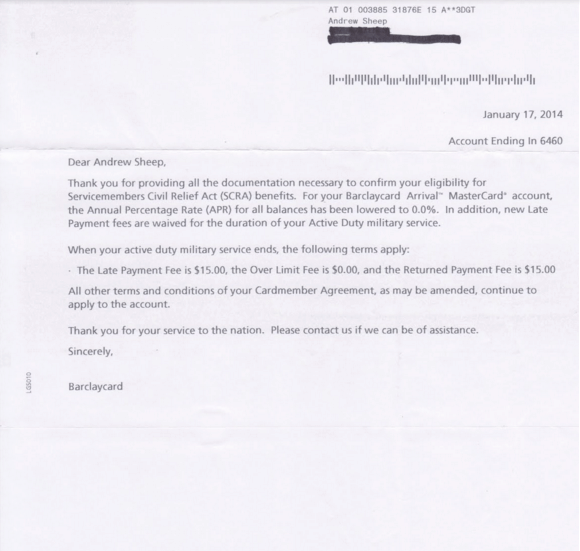

If you opened an account before active duty, Barclays Bank offers 0% APR and no annual fees on credit cards during active duty. However, members who began active duty and are now looking at a Barclays card will not be considered SCRA eligible and, therefore, are responsible for any fees and standard interest rates that apply to a card.

Contact Barclays at 1-888-710-8756 to get more information or to apply for benefits.

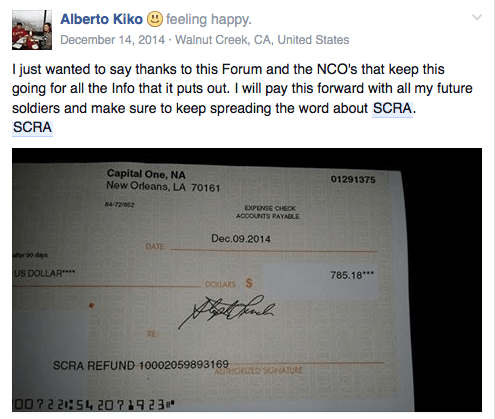

Capital One Bank

Under the Capital One SCRA Program, all fees are waived on all cards, and service members can enjoy 4% APR during active duty and for one year afterward.

It’s easy to apply for these benefits online or you can call 855-227-1645 to speak with a Capital One Military Specialist. This line is available 24/7.

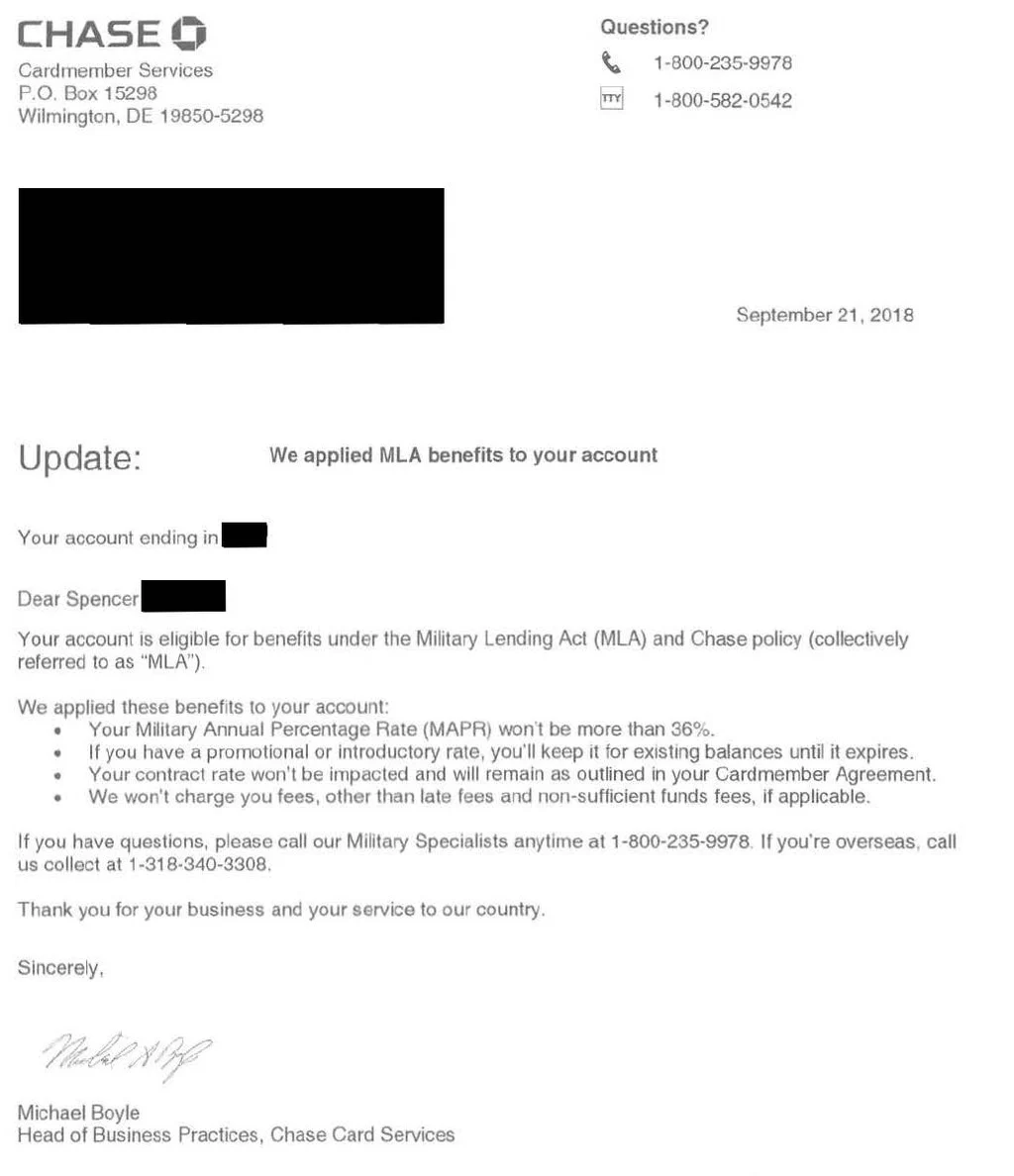

Chase Bank

Chase Bank will waive all fees and lower the APR to 4% on eligible balances and for one year after separation. On Chase Military cards, all interest and fees incurred during deployment will be refunded as part of Chase’s SCRA benefits program.

Call Chase Military Services at 877-469-0110 about these and other servicing benefits available to you. Specialists are available Monday – Friday from 8 am to 9 pm ET. If you’re calling internationally, call 1-318-340-3308.

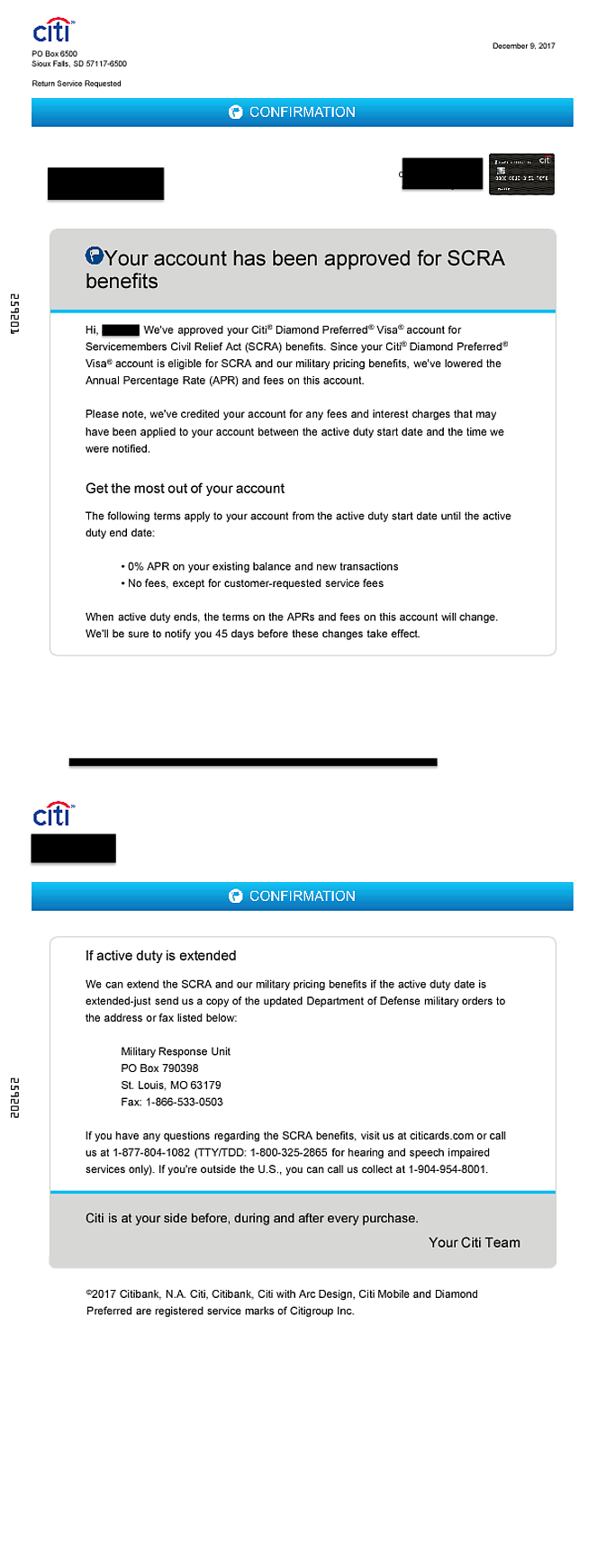

Citi

For accounts opened before active-duty service, Citi offers a 0% APR during active duty. They will also waive all fees on these accounts. Outside of active duty, standard variable APRs and rates apply.

To discuss benefit details, Call Citi’s military specialists 24/7 at 877-804-1082 in the U.S. and 605-335-2222 if you’re overseas.

You may also fax, mail or overnight/express delivery to the fax number and address for Citi listed below. Please ensure you also send the proper documentation – this could include a copy of your written Department of Defense (DoD) orders, a letter from your commanding officer, or any other document that the DoD deems a substitute for official orders.

For credit cards, mortgages, and other banking products from Citi:

Citi Customer Service

SCRA Unit

P.O. Box 790398

St. Louis, MO 63179

Fax: 1-866-533-0503

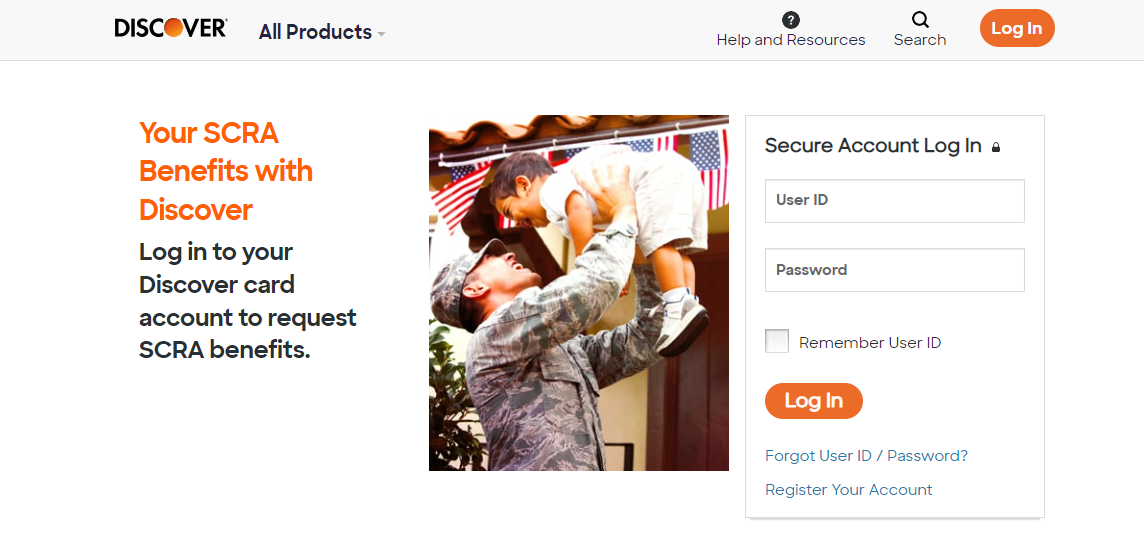

Discover Card

If eligible, Discover Card service members will receive an interest rate not exceeding 6% on debt incurred before active duty, including most fees, for the duration of the service member’s active duty.

There are several ways to apply for benefits.

- Online: Click ‘Request Benefits Now’ when securely logging in to your account.

- Phone: Call 1-844-DFS-4MIL (1-844-337-4645). If you are overseas, call 1-801-451-3730. (If your active duty time period is in the future, provide your active duty dates.)

- Mail: Discover Attn: SCRA Department P.O. Box 30907 Salt Lake City, UT 84130-0907

- Fax: Attn: SCRA Department 1-224-813-5767

Discover will attempt to verify active duty by contacting the Defense Manpower Data Center (DMDC). If verified, no documentation is required; however, service members are encouraged to submit documentation that may provide additional information.

Once activated, your SCRA benefits may automatically extend to other Discover products, such as personal loans, home equity, home loans, and student loans.

If the account is enrolled in Discover Payment Protection, you may be eligible to pause your monthly payments, interest fees, late fees, and Payment Protection fees during your call to active duty. You can call 1-800-290-9895 to speak to a specialist about pausing your payments.

First Command

First Command Bank specifically targets military families to assist them with a variety of financial issues. Nine out of 10 advisors are veterans or military spouses who are squarely focused on serving as personal financial coaches to service members and military families.

To discuss SCRA benefits, contact First Command at 800-763-7600.

Navy Federal Credit Union

Your Navy Federal accounts may be eligible for SCRA benefits if they were opened before you started active duty. This includes:

- Consumer loans

- Mortgages (including Home Equity Lines of Credit)

- Checking Lines of Credit

- Credit cards

- Business loans

- Student loans

You must request SCRA benefits from us no later than 180 days after your active duty end date. To get started, you’ll need to complete a Request Benefits form.

For your convenience, you can submit your form in any of the following ways:

By eMessage: You can easily send a message from your Navy Federal online account or from the mobile app. In the subject line, please write: ATTN: SCRA, Mortgage Servicing.

By Fax: Send your fax to 703-206-3108, ATTN: SCRA, Mortgage Servicing.

By Mail: Navy Federal Credit Union P.O. Box 3000 Merrifield, VA 22119, ATTN: SCRA, Mortgage Servicing.

Visit Your Local Branch: A branch representative will be happy to assist you in submitting your form and/or documents to SCRA.

Pentagon Federal Credit Union (PenFed)

SCRA benefits through Pen Fed are effective on the date your active duty begins and generally end on the date you are discharged or released from active duty. To apply for benefits, you’ll need to submit documentation.

Gather your activation orders. You can send your activation notice up to 180 days after the last date of your active military service. Upload your documents to PenFed.org/secureupload.

Pen Fed will review your request and let you know if more information is required.

If you have questions, you can submit a request for more information here or visit a branch to get answers.

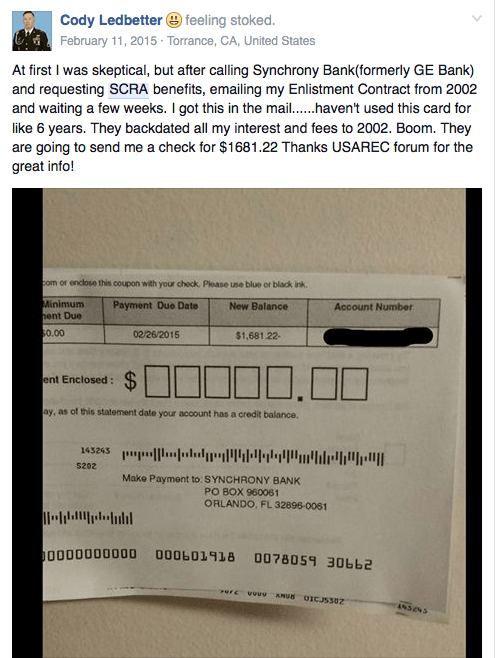

Synchrony Bank (formerly GE Capital)

Synchrony Bank will review all current and closed accounts under GE Capital and, if approved, reduce interest rates to 6% and waive all associated fees.

You may also be eligible for 0% interest from Synchrony Bank for new accounts created after joining military service.

Please fax your request, including active military orders or other documents, to (866) 694-6580 or mail it to Synchrony Bank, SCRA Dept, PO Box 965074, Orlando, FL 32896.

For details, contact Synchrony Bank at 1-855-872-4311 or 1-866-419-4096, and be ready to provide your social security number and a recent LES.

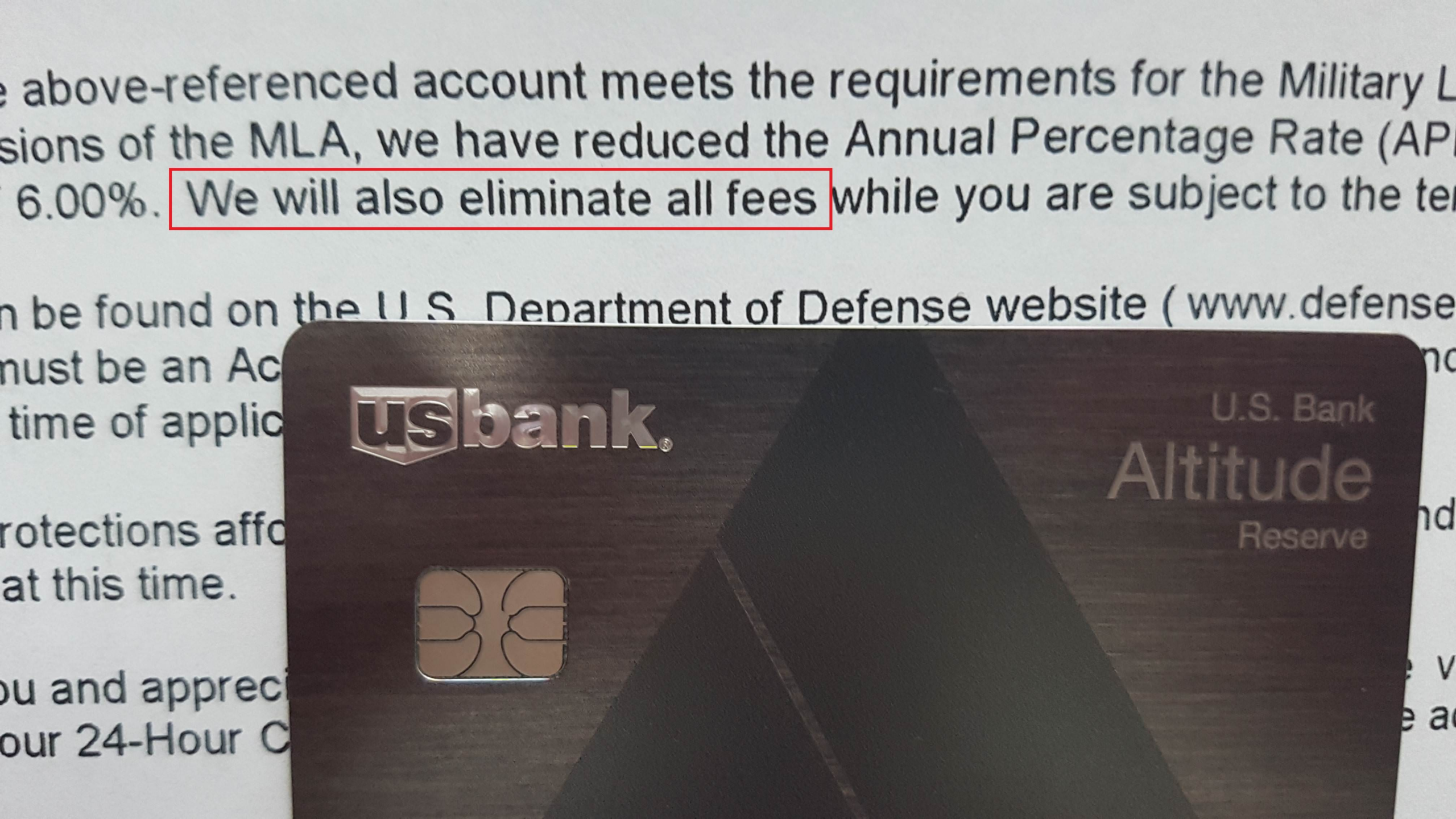

US Bank

While US Bank offers the required SCRA benefits, it does not offer special offers beyond what is required by law.

US Bank can help you understand your rights when you contact the Military Service Center and assist you with benefits.

Phone (in the U.S.): 800-934-9555

Phone (international collect): 513-277-5899

Email: [email protected]

Hours of Operation: Monday – Friday, 7 a.m. – midnight (ET)

USAA

USAA offers several servicemember-friendly benefits related to SCRA. These include

- A reduced interest rate of 4% on eligible credit card balances.

- Waiver of credit card account-related fees when approved for the program.

- Extension of approved benefits for one year after active duty end date.

Contact USAA at 800-531-USAA (8722) and request assistance.

Wells Fargo

Wells Fargo offers the required SCRA benefits but there are no special offers above and beyond what is required by law. To take advantage of SCRA benefits with Wells Fargo, sign on to Wells Fargo Online® to easily and securely upload your military service documentation.

You can also send your military service documentation through these other ways:

Mail/Overnight Mail:

Wells Fargo Bank

c/o SCRA Request

DSR – MAC D118-02M

1525 W. WT Harris Blvd.

Charlotte, NC 28262-8522

Fax:

1-855-872-6262

Wells Fargo branch

Find a location near you

Email:

For secure email options, call 1-855-USA-2WFB (1-855-872-2932).

For More Information

If you have questions about your SCRA or MLA rights, contact your nearest military legal office for more information.

Thanks for reading… If we’re missing any credit card companies, feel free to leave the specifics in the comments!

The Military Wallet has partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. Some or all of the card offers that appear on The Military Wallet are from advertisers. Compensation may impact how and where card products appear, but does not affect our editors’ opinions or evaluations. The Military Wallet does not include all card companies or all available card offers.