How Much Is Your Military Pay Really Worth?

Your military compensation is worth more than you think it is when you consider your base pay, tax-free income, healthcare, retirement benefits, and access to other benefits.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

For any servicemembers who are transitioning out of the military or perhaps daydreaming about what that might look like someday, many of them have never considered the full impact that transition will have on their finances and total compensation. Most of the servicemembers that I counsel are surprised after they separate and don’t have the same salary, benefits, or total compensation than they did in the military. What can you do about this if you’re set to separate or are thinking about it?

Every year, usually in early April, DFAS publishes the Personal Statement of Military Compensation (PSMC) with the intent to help make servicemembers’ full compensation more readily visible. While DFAS states that this may be helpful in applying for credit or loans, the true benefit lies in understanding what your equivalent compensation would need to be outside of the military to maintain your same standard of living.

Defining Compensation

In this context, compensation refers to the entire sum of salary, benefits, and other financial support that servicemembers receive. The majority is “direct compensation” — money paid directly to you — while the rest is called “indirect compensation” — things that financially benefit you but aren’t a direct payment. Indirect compensation can either be financial compensation or non-financial.

One example of indirect financial compensation is healthcare. When an employer helps pay for your healthcare coverage, that’s indirect financial compensation since you otherwise would have to pay that amount. Indirect compensation can also be non-financial like leave. Direct compensation is readily apparent because these are clearly listed on your LES while indirect compensation might not be as immediately clear. The goal of this post is to help you understand the full picture of all of your compensation.

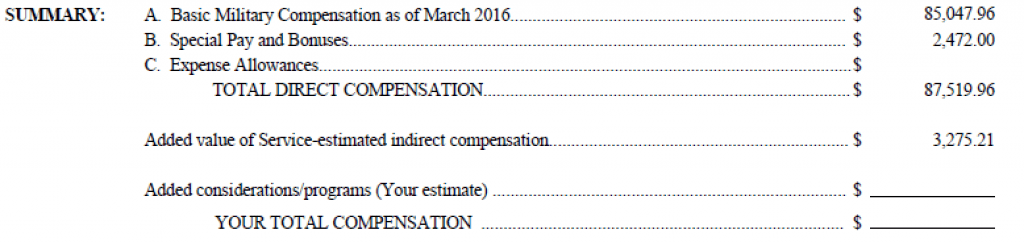

It’s important to take a look at each detail of the PSMC since each analysis can differ based on personal circumstances. You can access your PSMC through myPay right underneath where you can view your LES. This article will probably be most helpful if you have your own PSMC to go through. I will use my 2016 PSMC as the example for this post and show you how to analyze your own.

Direct Compensation

DFAS pre-fills in your basic pay, special pay and bonuses, expense allowances (OHA, COLA, etc.), as well as an estimate of the added value of indirect compensation which is usually based on the federal tax advantage of BAH and BAS. This provides the starting point for you to add in some personal analysis about all the indirect compensation and add your estimate back in at the end to get your total compensation figure.

Estimating Your Indirect Compensation

As you estimate the various forms of indirect compensation, don’t stress getting each figure down to the exact dollar amount. The goal is to gain a more complete understanding of what that benefit might cost you if you had to pay for it yourself so estimating is OK. It’s also usually best practice to estimate conservatively on these figures so you don’t have a highly inflated final compensation figure to compare against equivalent civilian compensation.

If you aren’t sure what a benefit is worth, ask friends or family for help especially if they aren’t in the military and they could give you a more realistic picture of what benefits are worth outside of the military. Below is an explanation of how you can go about calculating each of the indirect compensation categories on the PSMC.

How Taxes Impact Your Military Compensation

Taxes can have a significant impact on your total militay compensation. That is why tax planning is essential while you are serving in the military.

In my PSMC above, DFAS has estimated that based on my current BAH and BAS I am saving $3,275.21 a year by not paying federal income tax on those two allowances. Given that I’m also a resident of a no-income-tax state, that figure understates my total tax advantage as well. Were I to add state income tax for the state I would likely be living in into this calculation, I would be paying another approximately $2,500 a year in state income taxes just on basic pay alone.

Even though the PSMC doesn’t specifically tell you to calculate the state income tax until later on, I’m including it here in this section. State income taxes are especially relevant if you’re currently paying no state income tax, but will be moving post-military to a new state that has income tax.

Another thing to consider here is combat zone tax exclusion (CZTE). The PSMC doesn’t list this as part of the analysis, and it could easily be argued that this is a direct benefit to help offset some of the challenges of deployments. For many service members however, a deployment might mean going down one tax bracket from 15% to 10%. More senior servicemembers or dual-military could really reap benefits here if they own more significant taxable investments and drop from the 25% tax bracket to the 15% and its subsequent 0% tax rate on long-term capital gains and dividends.

Junior servicemembers could also drop below the income threshold to be eligible for the Earned Income Tax Credit (EITC) which could mean quite a bit of extra money at tax time. I personally don’t consider CZTE in my calculation, but others might choose to do so, especially if you deploy on a more regular schedule.

- Formula: (Projected) State Income Tax x Current Basic Pay = State Income Tax Benefit

- CZTE Formula: # of Months Deployed x Monthly Federal Tax Deduction = Benefit

Medical Care

Tricare is the biggest indirect financial compensation for most servicemembers and their families. For servicemembers who haven’t had a full-time job outside the military, most are insulated from what almost everyone else in the country has been going through over the last several years. Medical insurance can be incredibly expensive for many Americans so this area of compensation is critically important to understand.

Since servicemembers enrolled in Tricare Prime never see any costs that they have to pay for themselves and dependents on Prime have only small co-payments, this can hide the full Tricare benefit (except for those that read their Tricare Summary Explanation of Benefits and see what some of those medical benefits actually cost).

Tricare Select poses a slightly greater financial impact due to it having an annual deductible [$150 deductible/person or $300/family or (E-1 to E-4: $50/person, $100/family)] and a 20% cost-share for outpatient care. Even then though, Tricare Select only has a $1000 maximum out of pocket (MOOP) cost each year which means the most a family would pay towards their covered healthcare costs is $1,000 a year!

The big question is, how do you know how much Tricare is worth to you?

One way to measure this is to see how much it would cost you to buy Tricare Select coverage without the military paying for any of it. This option exists as the Continued Health Care Benefit Program (CHCBP) provided by Humana. Similar to COBRA, his plan can give you temporary health coverage for 18-36 months when you lose eligibility for Tricare. Basically it means that you pay 102% of the total insurance premiums which in this case were previously all paid for by the military.

In FY16, CHCBP premiums would be $1,849 per quarter for individual coverage and $4,621 per quarter for family coverage. In addition to these premiums, there will be yearly deductibles and cost-shares similar to Tricare Select. That comes out to a minimum of $7,396 (individual) or $18,484 (family) respectively a year. Plus, consider that is also a tax-free benefit so it’s worth even more than just an equivalent cash payout.

Another way to compare the value of Tricare is to see what health insurance coverage would cost you on the healthcare.gov exchanges. This gives you a very good example of how much you could otherwise be spending given your specific family circumstances as healthy, young individuals can acquire more minimal coverage much cheaper than CHCBP while families might see some major sticker shock.

In my family’s case, my wife has dealt with some health challenges which have made Tricare even more valuable to us. I estimate my Tricare benefit to be worth about $20,000 a year given what my wife and I would have to pay out of pocket between all costs on a typical civilian plan.

That extra $7,000+ of benefit beyond the $12,348 comes from the massive bargaining power that Tricare has to negotiate drug costs, the low MOOP of only $1,000 on Tricare Select vs. an expected MOOP of closer to $10,000 for insurance purchased on the healthcare exchange, and comparison of co-pays and cost-shares between Tricare and health insurance sold on the exchanges.

While Tricare changes are coming that will add a small annual premium in 2020 to Tricare Select, servicemembers will continue to receive some of the cheapest and best health insurance coverage in the country today. Practice expectations management prior to separating and don’t expect your health insurance to offer as much for as little as Tricare costs. The bottom line is this: don’t undervalue your Tricare coverage!

- Formula: Expected Annual Health Insurance Cost – What You Currently Pay Annually for Tricare Prime/Standard = Benefit

Military Pension

Until the new Blended Retirement System (BRS) starts, the current military retirement benefits only consist of the High-3 system as an all-or-nothing pension that requires vesting at 20 years of service.

Doug Nordman has done a great job giving some estimates of what that military pension is worth. The trick of course is that the pension is still worth “nothing” until you actually vest in it so there’s no real way to say you’ve earned half of the pension’s value just because you have served 10 years. To quote Nords, “Stay in the military if you’re challenged and fulfilled, but don’t join just to stick it out for a pension. If the pension is your only motivation then you won’t last past the first obligation. When the fun stops then you should leave active duty for the Reserves or National Guard instead of grimly clenching your jaw and gutting it out for 20.”

Still, it is critical to understand just how incredibly valuable an active duty military pension can be as an E-7 pension can be worth around $1.4 million at the time of retirement and an O-5 pension could be worth as much as $2 million! [calculations above used 2017 pay tables valuing the pension in today’s dollars]

This part of the PSMC analysis doesn’t produce a number to add into my overall compensation, but it does help me think through the calculus of staying in or getting out. The more years of service that each military member has should also weigh heavily in this consideration as it’s easier to make the decision to get out after only 4 years vs. 15 years.

Thrift Savings Plan

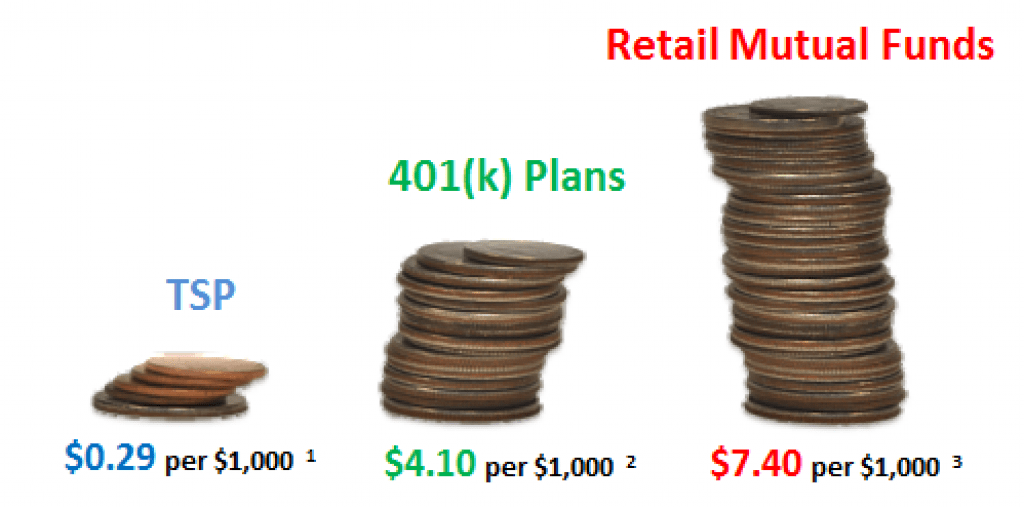

The TSP offers incredible cost savings as it is dramatically cheaper than the average expense ratio of traditional mutual funds. In 2015, the TSP had a net expense ratio of only 0.029% while the average expense ratio of the civilian TSP equivalent of a 401(k) and average mutual funds are much more expensive! That means that if your TSP balance is $1,000, you are only paying about $0.29 a year in fees while that same $1,000 in an average 401(k) would cost you $4.10 a year or even $7.40 inside an average mutual fund.

Over time, that fee differential becomes a huge drag on investment returns — to the tune of tens of thousands or even hundreds of thousands of dollars — which you can see for yourself using this Vanguard tool.

I use the fee differential from the average 401(k) since I assume that if I wasn’t in the military, I would also be contributing to the 401(k) what I now save in the TSP. Based on how much I have currently saved in the TSP and by continuing to max it out each year, I’m estimating that I save at least about $310 a year thanks to the low fees in the TSP.

- Formula: (Amount Currently in TSP x 0.0041) – (Amount Currently in TSP x 0.00029) = Benefit

Life Insurance, Dependency and Indemnity Compensation, and Survivor Benefit Plan

Let’s analyze SGLI, DIC, and SBP in the context of the actively serving member to apply this to the PSMC, but understand that these concepts also apply to military retirees albeit with some differences. Many companies offer some type of group life insurance that is tied directly to employment and SGLI functions just like this.

Although individual servicemembers pay for SGLI, this guaranteed insurance is still pretty low-cost, but most importantly helps ensure service members can stay insurable post-military with VGLI should something happen to them while in the military. These are the other benefits broken out:

- Should you pass away, your family or designated beneficiary will also automatically receive a death gratuity payment of $100,000 regardless of whether you have SGLI coverage or not.

- If your death is determined to be in the line of duty and if you are married, your spouse will also receive monthly non-taxable Dependency and Indemnity Compensation (DIC) payments of at least $1,254.19 and an additional $310.71 for each surviving child are payable. DIC is generally adjusted annually for inflation.

- The family will also receive one year of BAH based on the current rate they were previously receiving.

- If you die while on active duty in the line of duty, your family is protected by SBP at no cost to you. The formula for this looks like this: SBP = 0.55 x (2.5% x YOS x average of the highest 36 months basic pay). My formula comes out to 0.55 x (0.025 x 8 x $5,472) = $601.92. However, due to current federal law that governs the “SBP-DIC offset,” the SBP amount is reduced by the amount of the DIC. That means that my wife would get $0 of the $601.92 SBP payment because the DIC payment is more. For right now, Congress has a stop-gap measure in place until Oct 2017 that would allow $310 of the SBP benefit to be paid to my wife. So the total DIC and SBP to my wife would be $1,254.19 + $310 = $1,564.19 a month or $18,770.28 a year. Again, this is not a benefit that I have to pay for right now.

How much life insurance would I approximately need today in order to provide a $19,000 a year inflation-adjusted annuity for the rest of my wife’s life? I plug the requirements into the calculator here (I used ~3% for the interest rate as inflation) which says that annuity is worth about $509,000 in today’s dollars given my wife’s age and IRS expected life span.

That means I would need to carry an additional $609,000 ($509K + $100K death gratuity) in life insurance today to provide that same level of benefit to my wife. For the sake of estimating, I’ll use the SGLI rate of $0.07 per $1,000 of coverage à $609,000 x $0.00007 = $42.36 a month or $511.56 a year. [Note: I could potentially get a lower term life insurance rate than this rate given underwriting characteristics]

The equivalent costs of term life insurance vs. SGLI are usually easy to compare and many servicemembers often carry life insurance through companies like AAFMAA, USAA, or Navy Mutual. Many people though don’t think about pricing out the income streams that their families could also earn through DIC and SBP when considering their life insurance needs.

- Multipart Formula:

o If [0.55 x (0.025 x YOS x average of the highest 36 months basic pay)] > $1,245.19, then use that amount instead of the DIC Benefit of $1,254.19. Otherwise use $310 in place of your SBP.

o [($1,254.19 + $310 + $310.17 per child) x 12] OR [0.55 x (0.025 x YOS x average of the highest 36 months basic pay) x 12]

o Calculation above produces annual annuity present value figure à Plug into calculator here given 3% interest and your spouse’s life expectancy from today (See Appendix B, Table I). Round number up to nearest $10K increment.

o ($100,000 + Annuity Present Value Figure) x 0.00007 = Benefit

Pay Raises

The PSMC next has you calculate the value of annual pay raises, longevity increases, and promotion raises. While the annual raises haven’t really been keeping up with inflation lately, the longevity increases, and promotion raises both offer standardized opportunities for increases in pay. This one is a lot more difficult to measure though and depends on you remaining in the military so I skip it for this analysis.

One important consideration for you though might be the comparison here between regular raises in the military and whether or not your civilian career offers the same chances to regularly grow your pay.

Commissary and the Exchange

This category is very dependent on how much each family uses the Commissary and Exchange. The 2016 PSMC lists out that the average Commissary benefit is about $4,430 a year for a family of four with most people saving about 30% of their grocery purchases. More recent statistics as reported by Stars and Stripes show that figure to be about 24% on average now though and can vary widely between assignment locations.

In our particular case, we live off base pretty far from the Commissary and Exchange and can get very good deals through Costco, our local coop, community supported agriculture, buying meat directly from ranchers, and deal hunting online so I don’t calculate anything from this benefit. Take into your purchasing habits to fully analyze this one for you.

- Formula: [(Average Monthly Commissary Spending x 1.24) x 12] – [(Average Monthly Commissary Spending x 12] = Average Benefit

Note: To get a more accurate estimate, the Stars and Stripes article breaks out the average savings by region and can range from around 19% to over 44% for OCONUS.

Federal Long-Term Care Insurance Program

This benefit primarily offers long term care insurance for those looking to help cover the cost of nursing home and other end-of-life care. The goal of the Federal Long-Term Care Insurance Program (FLTCIP) is to help preserve your retirement savings should a long-term care need arise.

Those eligible for the FLTCIP include all Federal Employees (Uniformed Service members), their spouses, adult children (including natural, adopted & step), parents, parents-in-law, and stepparents. Given my current age, current and projected savings rate, and expected financial independence long before my 60s, I don’t have a need for this. Your situation may be different especially if your parents could purchase through this benefit program. I encourage everyone with older parents (55+) to at least make them aware of this program if weren’t familiar with it already.

- Formula: Other Annual Long Term Care Insurance Cost – FLTCIP Annual Cost = Benefit

Education Benefits

The military offers some pretty incredible education benefits through Tuition Assistance (TA), the GI Bill, ROTC scholarships, Academy appointments, job certifications, and other opportunities. I’ve written about that using my own example here where I figured out how I turned $80,000 of education benefits into more than $2.1 million in lifetime value!

The primary education benefit to account for here is TA or service-specific associate degree program since it is a function of remaining on active duty whereas the 9/11 GI Bill vests after 36 months of qualifying service (ROTC scholarship and Academy grads take note that you must first finish your education commitment before starting to earn credit towards the 9/11 GI Bill).

If you are currently still serving towards the 36 months to earn 100% of your benefits or are still serving an ADSC because you transferred the benefit to a dependent, include a pro-rated portion in the calculation below.

There will be lots of variation about how much the 9/11 GI Bill education benefits can be worth so I’m using $90,000 to approximate a 4 year undergraduate degree. Since I’m not currently using any TA having already leveraged this benefit for my first masters degree and have already vested my 9/11 GI Bill for myself, my calculation comes to $0 for my salary analysis. For your analysis, use the formula below.

- Formula: Total Annual TA + (Total Associate Degree Credit Hours x $250) + Pro-rated Time Percentage (I.e. 18 months served for 36 months = 50%) x $90,000 = Benefit

Service Activities

Everyone’s use of the services provided by their base will differ greatly so this is another highly personalized analysis. Among the most financially impactful is the child development center (CDC) since this cost is subsidized based on rank. For those that utilize the CDC, you can try to determine the cost of a similar daycare off base and compare the CDC cost to add up your benefit.

I only occasionally use some of the other service offerings like the library, clubs, and outdoor recreation. My biggest benefit comes from the fitness center that I would otherwise purchase off base. I estimate my total benefit here to be about $400 a year.

- Cost of Off Base Service – Cost of on Base Service = Benefit

Counseling and Assistance Programs

The PSMC helps provide some figures here ranging from $30 an appointment up to more than $5,000 for transition assistance services to help you analyze the costs for free personal financial management counseling, relocation services assistance, transition counseling, spouse employment consultation, and assistance from a wide range of services available from their services’ community centers.

Again, each individual circumstance will differ here. Based on what my wife and I use, this comes out to about $300 a year.

- Cost of Off Base Service – Cost of on Base Service = Benefit

Legal Counseling

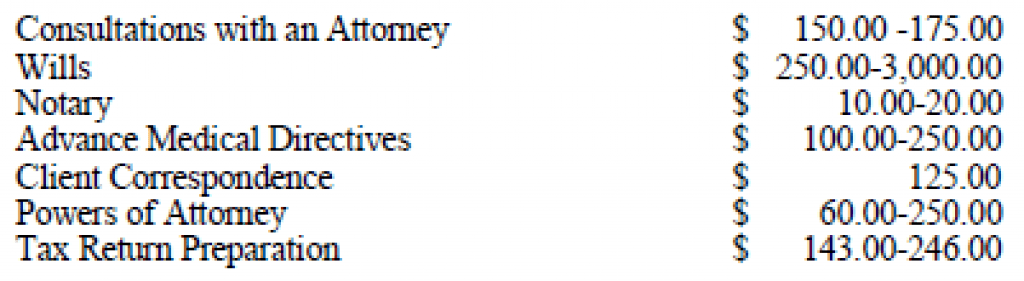

Military members and family members can get free legal assistance in a wide range of areas, including consumer law, landlord-tenant law, family law, estate planning, and tax assistance services. The PSMC again offers their estimates for costs associated with everything from notarization or powers of attorney to tax returns preparation and consultations with an attorney. My estimate for these services I use is about $400.

- Cost of Off Base Service – Cost of on Base Service = Benefit

Space-A Travel

Space available travel for Uniformed Services members can provide substantial savings over commercial airline fares. Space available travel is defined by DoD policy as a privilege (not an entitlement), which accrues to servicemembers as an avenue for travel. This is again a highly individual element likely based on how close you are to frequent space-a travel opportunities. In my case not much, so this benefit is a $0 for me (at least right now).

- Formula: Cost of Equivalent Ticket – Cost of Space-A Flight = Benefit

Tricare Dental Program

Tricare dental provides fairly good coverage, but is not quite the comparison as Tricare health insurance is compared to civilian counterparts. Based on equivalent quotes for comparable coverage, my wife could be covered by a similar plan where we live for about $30 a month. Since TDP costs $11.68 a month for her, that’s about $18 a month in benefit or about $216 a year.

- Formula: Comparable Dental Insurance Annual Cost – Annual Tricare Dental Program Cost = Benefit

Other Benefits

The PSMC stops its analysis here, but there are a few other benefits to consider.

- Leave: The average civilian job has much less paid time off (PTO) than the annual 30 days of leave a year each and every servicemember receives. Although I’ve never met someone who only uses that leave to take a month straight off each year, in effect you are getting paid 12 months’ worth of salary for 11 months of work.

Military life demands many more sacrifices on your time (TDYs, deployments, long shifts, etc.) and there’s certainly no such thing as overtime so perhaps this issue ultimately is a wash. However, don’t discount the amount of paid time off you do get lest you be surprised when your civilian job starts out with only around 5 days a year. Expectant or future mothers should especially value the recent increase in military maternity leave as it outpaces most companies in the country as this is a rarer benefit.

In my case, I evaluate this benefit as a financial wash given some of the other constraints on my time.

- Disability Insurance (DI): At most other jobs either your company offers some small level of disability insurance or you can purchase this on your own. While most people might not know what disability insurance covers, they have probably seen this product advertised somewhere thanks to a famous quacking duck.

Disability insurance is coverage that will help pay a reduced portion of your previous salary if you were to get hurt or otherwise be unable to work anymore. In the military, this is provided by theVA if you were to become seriously injured or disabled while serving in the military. You would be evaluated and given a disability rating which would then be used to determine how much you get paid.

I would otherwise have to purchase a DI policy on my own to provide this coverage. The average cost for a disability income insurance policy is around 1% – 3% of your annual income (take note that most policies will only allow you to purchase around 65% of your previous salary). You would have to get a personalized quote from an insurance agent to get more details. My rough “guessestimate:” $87,000 x 0.02 = $1,740 à for an annual benefit of $56K

Formula: Current Pay (Basic Pay + BAH + BAS) x 0.02 = Benefit

- VA Benefits: Outside of the VA benefits specifically mentioned already, there are a host of other benefits available such as the VA loan, education and career counseling, VA medical resources, and other support. Evaluate what services you already use or might expect to use when you separate for an estimate here. You can even use the PSMC estimates back from the counseling assistance programs for financial impact. In my case, I save the cost of private mortgage insurance (PMI) on my VA loan which saves me around $1,800 a year. Now since I’ve already qualified (vested) for my VA benefits, I won’t count this figure into my PSMC calculations, but it is still a really great help.

- Military Discounts: You may never have considered this one, but this perk can really add up as long as you remember to ask about it wherever you shop. During my first year of marriage, my wife and I figured out we saved almost $2,000 thanks to the cumulative effects of the military discount where we shopped. This benefit again is highly dependent on how much you spend and if the places you shop offer it.

Formula: Total Annual Spending at Merchants that offer Military Discount x Average Discount = Benefit

- Invaluable Camaraderie and Leadership Experiences: This consideration isn’t here to try and put a financial number on this one. However, one of the biggest trend items from separating veterans is how they miss the close bonds of friendship that are often more like family for most. You need to have realistic expectations that your average civilian employer will have a different (not inherently bad) culture in this area.

Pay and Benefits Summary

Let’s add up all my calculated numbers to see what my total estimated annual compensation is:

- Basic Pay = $85,047.96

- Special Pay = $2,472

- Total Direct Compensation = $87,519.96

- PSMC estimate of indirect compensation (federal income tax benefit of BAH/BAS) = $3,275.21

- State Income Tax = $2,500

- Tricare = $20,000

- TSP = $310

- DIC and SBP = $511.56

- Pay Raises = $0

- Commissary and Exchange = $0

- Federal Long-Term Care Insurance Program = $0

- Education Programs = $0

- Services Activities = $400

- Counseling Assistance = $300

- Legal Help = $400

- Space-A = $0

- Tricare Dental = $216

- Military Leave = $0

- Disability Compensation Insurance = $1,740

- VA Benefits = $0

- Military discounts = $2,000

- Total Indirect Compensation Estimate = $31,652.77

The Bottom Line

My Total Estimated Compensation = $87,519.96 + $31,652.77 = $119,172.73

Service in the military can bring with it quite a lot of financial benefits that are often underappreciated or not considered when evaluating total compensation. In fact, most servicemembers earn more in total compensation than their civilian counterparts when you consider similar levels of education and experience.

After this article, I trust you are better able to understand and analyze your PSMC. This can then help you evaluate equivalent civilian employment opportunities or perhaps even come to the realization that you’re better off staying the military for now. In any case, make sure to appreciate each of these benefits now whether you’re getting out soon or will stay for a whole career. In my case, it’s pretty interesting to realize that my total compensation is significantly higher than what my LES says!

I may have missed something else you might consider in your analysis so let me know what you think!

Footnotes to the TSP expenses image:

1 Net cost to TSP participants in 2015, averaged across all funds

2 All-in, participant-weighted cost of large 401(k) plans. Source: Deloitte, Inside the Structure of Defined Contribution/401(k) Plan Fees, 2013

3 Asset-weighted average expense ratio for equity mutual funds. Source: Investment Company Institute, 2014 Investment Company Factbook

Average Military Retirement Pay

There are several factors that determine your retirement pay but typically you can expect to recieve about half of your base pay when you retire. That equates to around $30,000 to $35,000 per year for typical enlisted personnel and about $60,000 to $70,000 for the typical officer.

Those estimates are based on serving full time active duty for an entire military service career. Service members retiring from the reserve can expect their retirement pay to be based on grade, tenure and total points earned for the periods worked.

What Branch Pays the Most?

All members of the armed forces, regardless of which branch you serve in, are paid according to rank, time in service, location of duty station, family members and job specialty.

For example, the lowest-ranking enlisted member, whether a United States Army Private or a U.S. Navy Seaman Recruit, has a pay grade of E-1. The highest-ranking officer, regardless of branch, carries a pay grade of O-10.

A slightly different way to look at where you’ll get the most pay is to compare which branch promotes the fastest, which leads to more pay. In general, the U.S. Army is the branch of the military that promotes the fastest.

However, there’s also individual initiative that can influence pay as well. Your military job and the level of advanced education you have will impact your ability to be promoted. A college degree can help you get promoted more rapidly, regardless of the branch you’re in.

Another thing to consider is that specialized career fields often don’t promote quickly. Branches typically promotes military personnel when those in higher ranks are promoted or retire or when they need more people in a particular field.

Is 20 Years in the Military Worth It?

That’s a highly personal question and only you can answer it. Life will throw you a lot of changes over 20 years and what seemed like a sure and solid career path at 25 might not have the same allure at 35.

On the other hand, if you value stability, interesting work, and are committed to serving your country, 20 years can fly by quickly. After 20 years, you’re still young enough to have a second career and chances are you’ve picked up some valuable skills along the way, as well as qualifying for a pension that will provide for you and your family for the rest of your life.

Keep in mind that you get alot of perks with military life and you may not be ready for the sticker shock of life after you complete your military career. Housing allowances, generous health benefits, career stability, insurance costs, pension and retirement considerations, and other similar hard and soft benefits are nowhere near as costly as they are when you’re a civilian.

You must weigh those options vs. some of the downsides of remaining as a service member. You may be able to get a higher paying job as a civilian, and there’s a really good chance you’ll be able to stay in one place for several years, instead of globetrotting from one duty assignment to another.