Military to Civilian Transition Tips (Podcast 17)

Transitioning from the military is difficult. You often hear about the success stories, but you rarely hear about the struggles. While my transition was ultimately successful, it wasn't easy. In this article and podcast, I share the struggles I had when I left the military, what I did to overcome them, and what I would do differently if I had to do it again.

Why trust The Military Wallet? We’re a veteran-founded resource that has helped millions make strong financial decisions.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers. You can read more about our card rating methodology here.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy.

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

Why I Struggled with my Transition

Here are some brief notes from my story:

Why I separated from the Air Force. I left active duty after 6.5 years on active duty. I was burned out from 5 deployments plus a one year special duty assignment in which I traveled around the world for an entire year. I was away from my home station for well over half the time I was in the Air Force. It was an amazing experience because I was young and single at the time, but I was ready for a change.

How I prepared for my separation. I had already achieved my bachelor’s degree while I was on active duty. This was discussed in podcast 8 – Tuition Assistance Benefits. This gave me the confidence to step out on my own into the civilian sector, even though I was planning on moving into a different career field. I had also saved a lot of money during my travels and deployments. I had several months worth of living expenses saved, and no large bills to hold me down.

Why I struggled with the transition. The transition was difficult for me. It took me 6 months to find a job which was difficult, but not for the reasons I had expected. I was financially prepared to go without income for several months (plus I was receiving unemployment benefits). The most difficult aspect of being unemployed was was losing my identity that I had associated with my role in the Air Force, and not being a part of something bigger than myself. This is a common thread among many veterans I have spoken with about the transition. And the longer you are in the military, the more difficult it can be to make the transition. The military is a unique way of life and it is a large part of people’s lives – too large to immediately replace with another job. Many veterans underestimate the emotional aspects of leaving the military. Please don’t make the mistake I made!

My first post-military job. My first job after leaving the Air Force was actually as a civilian contractor on an Air Force installation. This was a huge blessing for me, because it put me right back into the military environment. My Air Force experience was instrumental to me landing that job, and it helped me leverage the success from that position into a raise and a new title when I moved to a new company almost two years later. Even though I wore a suit and tie to work instead of a camouflage uniform, I was still part of a mission I understood and identified with. This was a key part of me starting to turn things around both personally and professionally.

Here are some brief notes from my story:

Why I separated from the Air Force. I left active duty after 6.5 years on active duty. I was burned out from 5 deployments plus a one year special duty assignment in which I traveled around the world for an entire year. I was away from my home station for well over half the time I was in the Air Force. It was an amazing experience because I was young and single at the time, but I was ready for a change.

How I prepared for my separation. I had already achieved my bachelor’s degree while I was on active duty. This was discussed in podcast 8 – Tuition Assistance Benefits. This gave me the confidence to step out on my own into the civilian sector, even though I was planning on moving into a different career field. I had also saved a lot of money during my travels and deployments. I had several months worth of living expenses saved, and no large bills to hold me down.

Why I struggled with the transition. The transition was difficult for me. It took me 6 months to find a job which was difficult, but not for the reasons I had expected. I was financially prepared to go without income for several months (plus I was receiving unemployment benefits). The most difficult aspect of being unemployed was was losing my identity that I had associated with my role in the Air Force, and not being a part of something bigger than myself. This is a common thread among many veterans I have spoken with about the transition. And the longer you are in the military, the more difficult it can be to make the transition. The military is a unique way of life and it is a large part of people’s lives – too large to immediately replace with another job. Many veterans underestimate the emotional aspects of leaving the military. Please don’t make the mistake I made!

My first post-military job. My first job after leaving the Air Force was actually as a civilian contractor on an Air Force installation. This was a huge blessing for me, because it put me right back into the military environment. My Air Force experience was instrumental to me landing that job, and it helped me leverage the success from that position into a raise and a new title when I moved to a new company almost two years later. Even though I wore a suit and tie to work instead of a camouflage uniform, I was still part of a mission I understood and identified with. This was a key part of me starting to turn things around both personally and professionally.

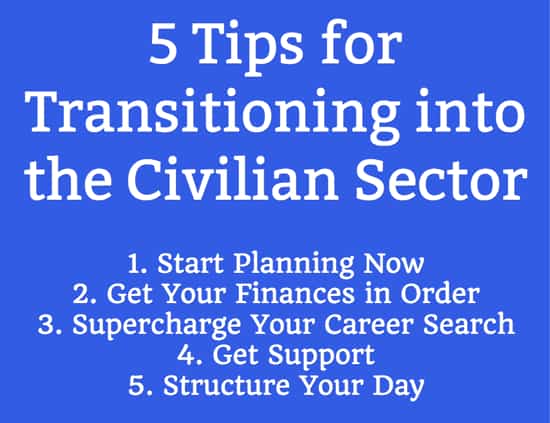

5 Tips for Transitioning into the Civilian Sector

1. Start Planning Immediately. Everyone leaves the military. It could be after 4 years, or 10 years, or 20 years, or even 30. It doesn’t matter how long you served, there will be a transition period for you – even if you walk right into a new job, or even if you think you won’t miss it (you will). The best way to handle this period is to start planning now, before you even know when you will get out of the military. Even though my transition wasn’t perfect, this was one thing I did well. I spoke with Mark Deal about this topic in Podcast 7, when we discussed planning your military exit. We both had similar ideas regarding planning – the idea is to give yourself a variety of options so you have options when you need to make a major decision.

Education is a big one – Mark and I both worked on our degrees while we were serving on active duty. You can do this by taking classes with tuition assistance, or even testing out of classes. Earning professional certifications or licenses is another great way to improve your military career and give you opportunities after you leave the military. There are a variety of certifications and licenses that are related to military career fields, and in many cases you can use your Tuition Assistance or GI Bill to earn those qualifications while you are still serving on active duty.

2. Get Your Financial House in Order. I can’t stress enough how important it is to get your finances in order before your transition. As I mentioned, money was not an area where I struggled during my transition. But that is because I was young and single, and I had been able to put away a lot of cash while I was deployed. Those who have a family and bills will have a more difficult time than I had. So it’s imperative to start planning now. You may be eligible for retirement benefits if you aren’t retiring (most retirees are ineligible for unemployment benefits because they are receiving a pension). But unemployment benefits don’t pay out very much. They will be helpful, but they certainly won’t cover all your expenses.

It’s difficult to give specific advice when everyone is coming from a different background and situation, so I’ll use general terms here:

1. Start Planning Immediately. Everyone leaves the military. It could be after 4 years, or 10 years, or 20 years, or even 30. It doesn’t matter how long you served, there will be a transition period for you – even if you walk right into a new job, or even if you think you won’t miss it (you will). The best way to handle this period is to start planning now, before you even know when you will get out of the military. Even though my transition wasn’t perfect, this was one thing I did well. I spoke with Mark Deal about this topic in Podcast 7, when we discussed planning your military exit. We both had similar ideas regarding planning – the idea is to give yourself a variety of options so you have options when you need to make a major decision.

Education is a big one – Mark and I both worked on our degrees while we were serving on active duty. You can do this by taking classes with tuition assistance, or even testing out of classes. Earning professional certifications or licenses is another great way to improve your military career and give you opportunities after you leave the military. There are a variety of certifications and licenses that are related to military career fields, and in many cases you can use your Tuition Assistance or GI Bill to earn those qualifications while you are still serving on active duty.

2. Get Your Financial House in Order. I can’t stress enough how important it is to get your finances in order before your transition. As I mentioned, money was not an area where I struggled during my transition. But that is because I was young and single, and I had been able to put away a lot of cash while I was deployed. Those who have a family and bills will have a more difficult time than I had. So it’s imperative to start planning now. You may be eligible for retirement benefits if you aren’t retiring (most retirees are ineligible for unemployment benefits because they are receiving a pension). But unemployment benefits don’t pay out very much. They will be helpful, but they certainly won’t cover all your expenses.

It’s difficult to give specific advice when everyone is coming from a different background and situation, so I’ll use general terms here:

- The priority should be reducing your fixed expenses as much as possible. The less money you have going out each month, the easier it is to deal with a change of income. Try minimizing as much debt as possible and reducing expenses you can do without on a temporary basis, such as cable TV, eating out frequently, and minor luxuries.

- You need to save money. It took me 6 months to find a job. A big reason it took so long is because I was looking for a job in a new career field. I was an aircraft mechanic in the Air Force, and I was looking for an office job. I found it, but it wasn’t easy, and it took a long time. You may be one of the lucky few who walks into a job a couple weeks after you leave the military, or you could be like me, and it might take several months before you find meaningful employment. Either way, you will need money to help you bridge the gap. As I mentioned unemployment benefits are available for many, but they might not be enough. I recommend trying to save at least 3 months of living expenses if you can. Between your savings and unemployment benefits, you should have a decent runway to get you through a rough patch. If you can save more, then go for it.

- Put off major purchases in the months leading up to your transition. You don’t want to be saddled with a new mortgage payment or a large car payment when you are going through a major career change. Waiting until after your transition will help your bottom line and reduce your stress levels.

- Continued membership in the greatest military in the world (not being part of a mission was a huge reason why I struggled with the transition).

- Continued pay and benefits. The pay is only for a couple days a month, but even a few hundred dollars (on up) can make a huge difference when you are out of work. The benefits are also nice. TRICARE Reserve Select is around $200 a month for a family plan and the co-pays and deductibles are very low. This is incredibly inexpensive compared to virtually all civilian insurance plans.

- Continue earning Points toward a military retirement. Very few companies now offer a pension plan, and the military has one of the best. A Reserve Retirement is still a very valuable thing to have, with the pension, health care benefits, and other benefits.

- Grow your professional network. Guard and Reserve units are like having another family. You will quickly meet new people and through them, your professional network will grow. I know several people who have found jobs through contacts in their Guard units. I can guarantee you will find a job through your unit, but it’s better than sitting at home (like I did!).